Table of Contents

Introduction

The GST appeal condonation of delay mechanism serves as a crucial lifeline for taxpayers who miss the statutory timeline for challenging adverse orders under the Goods and Services Tax regime. Understanding this provision becomes essential when taxpayers find themselves beyond the prescribed three-month limitation period for filing appeals under Section 107 of the Central Goods and Services Tax Act, 2017. The condonation of delay provision acknowledges that genuine circumstances can prevent timely compliance, offering a structured pathway for relief while maintaining the integrity of the appellate process.

With the recent amendments, the GST appeal framework has undergone significant refinements, particularly in the digital filing procedures and acknowledgment mechanisms. This comprehensive analysis explores every aspect of the condonation process, from the fundamental legal provisions to the latest judicial interpretations and practical compliance strategies.

Legal Framework for GST Appeal Condonation of Delay

Section 107 of the CGST Act: The Foundation

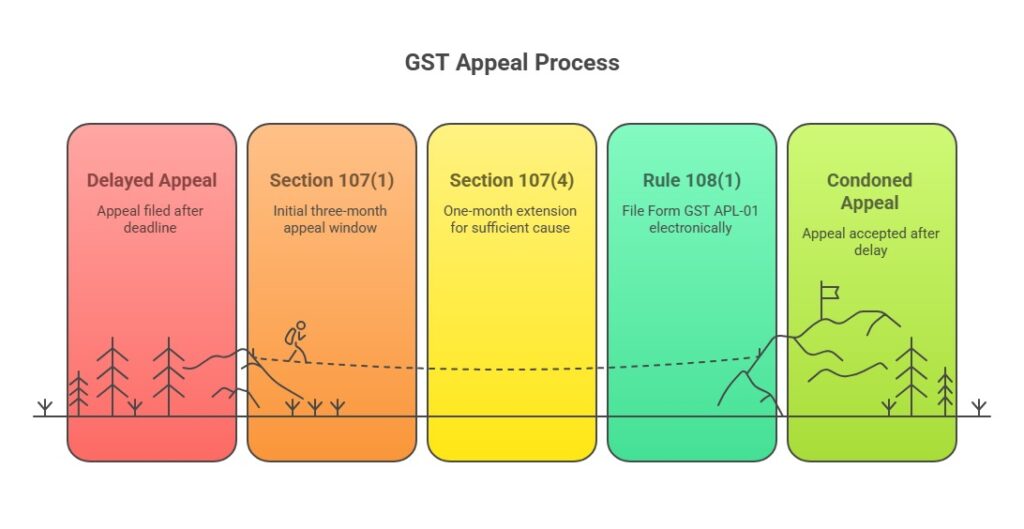

The cornerstone of GST appeal condonation of delay lies in Section 107 of the Central Goods and Services Tax Act, 2017. This provision establishes a comprehensive framework for appellate proceedings, with specific emphasis on time limitations and discretionary relief mechanisms.

Section 107(1) mandates that any person aggrieved by a decision or order passed by an adjudicating authority may file an appeal to the prescribed Appellate Authority within three months from the date of communication of the order. The critical aspect here is the phrase “from the date of communication,” which has been subject to extensive judicial interpretation.

Section 107(4) provides the statutory basis for condonation, stating that the Appellate Authority may allow an appeal to be presented within a further period of one month if satisfied that the appellant was prevented by sufficient cause from presenting the appeal within the initial three-month period.

Rule 108 and Form APL-01: Procedural Requirements

Under the Central Goods and Services Tax Rules, 2017, Rule 108 prescribes the procedural aspects of filing appeals. The 2025 amendments have introduced significant changes to the appeal filing mechanism:

Rule 108(1) now mandates that appeals be filed in Form GST APL-01 electronically through the GST portal. The provisional acknowledgment is issued immediately upon filing, but the appeal is considered filed only upon issuance of the final acknowledgment containing the appeal number.

Key Points:

- Mandatory digital filing through the GST portal

- Standardized use of Form APL-01 for all appeals

- Certified copy upload requirement for acknowledgment

- Enhanced documentation requirements for condonation applications

Time Limits and Calculation Matrix

Primary Limitation Period

The GST appeal condonation of delay framework operates within a structured timeline:

Period | Duration | Legal Basis | Remarks |

Primary Appeal Period | 3 months | Section 107(1) | From date of communication |

Condonation Period | 1 month | Section 107(4) | Subject to sufficient cause |

Total Maximum Period | 4 months (120 days) | Combined provision | Absolute outer limit |

Calculation of Limitation Period

The limitation period commences from the “date of communication” of the order, not the date of passing the order. This distinction has been clarified through various judicial pronouncements, including the recent Rajasthan High Court decision in V.R. India Trader v. State of Rajasthan.

Critical Considerations:

- Communication includes both physical and electronic delivery

- Service through registered post is complete upon delivery

- Electronic communication is deemed complete upon successful transmission

- Weekends and public holidays are included in the calculation

Sufficient Cause for Condonation

Definition and Interpretation

While the CGST Act does not define “sufficient cause,” judicial precedents have established comprehensive criteria for determining what constitutes valid grounds for condonation. The concept draws from the principles established under Section 5 of the Limitation Act, 1963, and various Supreme Court judgments.

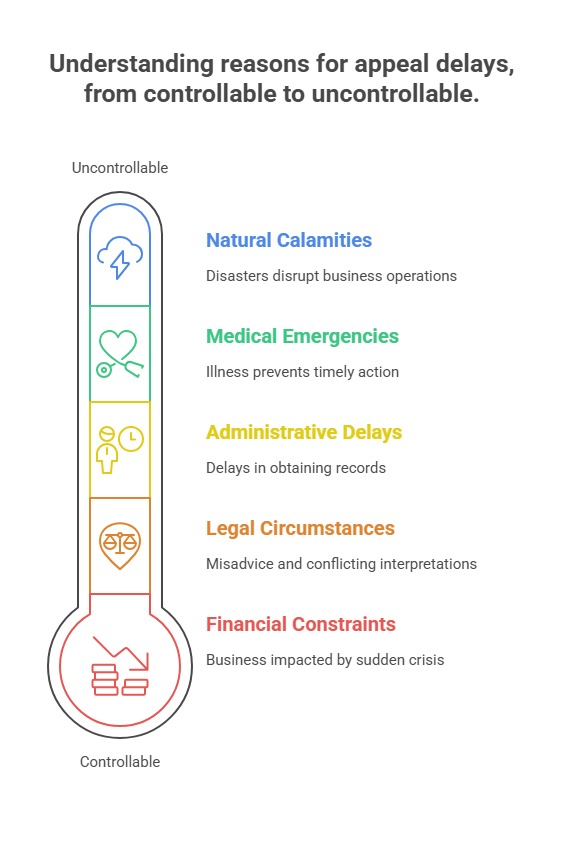

Recognized Grounds for Sufficient Cause

Medical Emergencies and Serious Illness

- Hospitalization of the appellant or immediate family members

- Serious medical conditions preventing timely action

- Mental incapacity or temporary disability

- Documentary evidence from qualified medical practitioners required

- Administrative and Procedural Delays

- Delay in obtaining certified copies of orders

- Non-availability of complete records from authorities

- Postal delays in delivery of orders

- Technical glitches in the GST portal

- Natural Calamities and Force Majeure Events

- Floods, earthquakes, cyclones, or other natural disasters

- Government-imposed lockdowns or restrictions

- Infrastructure failures affecting normal business operations

- Pandemic-related disruptions (as recognized during COVID-19)

- Legal and Professional Circumstances

- Legal misadvice from qualified professionals

- Conflicting legal interpretations

- Pending related proceedings in other forums

- Genuine mistake in understanding legal provisions

- Financial and Practical Constraints

- Sudden financial crisis affecting the business

- Absence of key personnel due to unavoidable circumstances

- Technical failures in communication systems

- Genuine oversight in record maintenance

Judicial Standards for Evaluation

Courts have established specific standards for evaluating sufficient cause:

Bona Fide Intention: The delay must result from genuine circumstances, not deliberate negligence or procrastination.

Reasonable Diligence: The appellant must demonstrate reasonable efforts to comply within the prescribed time.

Proportionality: The cause must be proportionate to the length of delay.

Contemporaneous Evidence: Supporting documentation must be contemporaneous to the events causing delay.

Documentation Requirements for Condonation Application

Essential Documents

- Condonation Application

- Detailed explanation of circumstances causing delay

- Chronological sequence of events

- Supporting evidence for each claim

- Verification by authorized signatory

- Medical Certificates (if applicable)

- Certificates from qualified medical practitioners

- Hospital discharge summaries

- Medical reports indicating inability to attend to legal matters

- Pharmacy bills and prescription records

- Administrative Correspondence

- Applications for certified copies

- Acknowledgments from authorities

- Postal receipts and delivery confirmations

- Email exchanges with officials

- Natural Calamity Documentation

- Government notifications regarding disasters

- Insurance claims related to the event

- Newspaper reports or official statements

- Photographs or videos of affected areas

- Professional Advice Records

- Legal opinions from qualified practitioners

- Chartered Accountant certificates

- Correspondence with tax consultants

- Fee payment receipts for professional services

Quality Standards for Documentation

Authenticity Verification:

- All documents must be original or certified copies

- Attestation by authorized persons where required

- Proper authentication of electronic documents

- Cross-verification with issuing authorities

Completeness Assessment:

- No gaps in the chronological sequence

- Adequate explanation for each day of delay

- Supporting evidence for all claims

- Proper indexing and organization

Judicial Precedents and Case Law Analysis

Recent High Court Decisions (2024-2025)

Calcutta High Court Decisions:

Mukul Islam v. The Assistant Commissioner of Revenue [2024]. The court held that the appellate authority failed to exercise jurisdiction properly in refusing to consider the condonation application. The case established that authorities must examine each condonation request on its merits rather than dismissing them summarily.

Sanyukta Bhattacharjee v. Union of India [2024]. This judgment clarified that explanations provided under Section 5 of the Limitation Act principles apply to GST appeals. The court emphasized that satisfactory explanations for delay must be accepted when supported by evidence.

Gour Mohan Bera v. The State of West Bengal [2024]. The court directed that there is no bar on considering condonation applications under Section 5 of the Limitation Act principles. The appellate authority must provide proper hearing opportunities before rejecting such applications.

Delhi High Court Ruling:

White Mountain Trading Pvt. Ltd v. Additional Commissioner [2024]. The court held that Commissioner Appeals erred in not considering the condonation application solely on the ground that it was beyond the period prescribed under Section 107(4). The matter was remanded for proper consideration.

Punjab and Haryana High Court Decision:

Vasudeva Engineering v. The Union of India [2024]. This landmark judgment addressed 17 writ petitions challenging rejection of appeals due to delayed filing. The court invoked Article 226 to condone delay, emphasizing that rigid timelines should not preclude access to remedies when pre-deposit requirements are met.

Rajasthan High Court Ruling:

V.R. India Trader v. State of Rajasthan [2024]. The court quashed the Appellate Authority’s order dismissing an appeal as time-barred, clarifying that limitation under Section 107 begins from the date of communication, not issuance. The decision emphasized the importance of proper communication procedures.

Emerging Judicial Trends

Liberal Interpretation of Sufficient Cause: Recent decisions show courts adopting a more liberal approach toward condonation, particularly in cases involving technical issues, administrative delays, and pandemic-related disruptions.

Emphasis on Substantive Justice: Courts are prioritizing substantive justice over technical compliance, especially when taxpayers demonstrate genuine intent to comply and present meritorious cases.

Procedural Safeguards: Judgments increasingly emphasize the need for appellate authorities to provide adequate hearing opportunities before rejecting condonation applications.

Step-by-Step Guide: How to File GST Appeal

Step 1: Pre-Filing Assessment and Documentation

Document Collection Phase: Begin by gathering all essential documents including the original order being appealed, proof of communication date, and evidence supporting grounds for condonation. Create a chronological file documenting every event that led to the delay in filing the appeal.

Grounds Evaluation: Assess whether your case meets the “sufficient cause” criteria established under Section 107(4) of the CGST Act. Document all circumstances that prevented timely filing, ensuring you have supporting evidence for each claim.

Pre-deposit Calculation: Under Section 107(6), calculate the mandatory pre-deposit amount, which is typically 10% of the disputed tax amount or penalty, subject to specified limits. Arrange the required funds before initiating the filing process.

Step 2: GST Portal Access and Form Selection

Portal Login: Access the GST portal (www.gst.gov.in) using your registered credentials. Navigate to the “Services” section and select “Appeal” from the dropdown menu.

Form APL-01 Selection: Choose Form GST APL-01 for filing your appeal. The 2025 amendments mandate exclusive use of this digital form for all appellate proceedings.

Step 3: Form APL-01 Completion Process

Section A – Appellant Details: Enter complete details of the appellant including GSTIN, legal name, address, and contact information. Ensure all information matches your GST registration records.

Section B – Order Details: Provide comprehensive details of the order being appealed, including order number, date of order, date of communication, and issuing authority details.

Section C – Grounds of Appeal: Articulate specific grounds for challenging the order with reference to relevant legal provisions. Be precise and avoid generic statements.

Section D – Condonation Application: This critical section requires detailed explanation of circumstances causing delay. Provide day-wise explanation for the delay period and attach supporting documents.

Step 4: Document Upload and Verification

Mandatory Uploads: Upload certified copy of the appealed order, proof of pre-deposit payment, and all supporting documents for condonation. Ensure file sizes comply with portal specifications.

Document Authentication: All uploaded documents must be properly authenticated. Original documents should be retained for potential verification during hearings.

Step 5: Pre-deposit Payment and Confirmation

Payment Gateway Access: Complete the pre-deposit payment through the integrated payment gateway. Acceptable payment methods include net banking, debit cards, and NEFT/RTGS.

Payment Verification: Verify successful payment completion and download the payment receipt. This receipt is essential for generating the final acknowledgment.

Step 6: Final Submission and Acknowledgment

Form Validation: The system performs automatic validation of all entered data. Resolve any validation errors before final submission.

Acknowledgment Generation: Upon successful submission, the system generates a provisional acknowledgment immediately. The final acknowledgment with appeal number is issued after document verification.

Step 7: Post-Filing Compliance and Follow-up

Status Monitoring: Regularly check the appeal status through the GST portal. The system provides real-time updates on processing stages.

Response to Queries: Respond promptly to any clarification requests from the appellate authority. Maintain proper communication records for future reference.

Beyond Statutory Limits: High Court Remedies

Article 226 Jurisdiction

When appeals are filed beyond the 120-day maximum period, the only remedy lies in approaching High Courts under Article 226 of the Constitution. This extraordinary jurisdiction is exercised sparingly and only in exceptional circumstances involving gross miscarriage of justice, factors completely beyond taxpayer control, or when no alternative remedy exists.

Recent High Court decisions demonstrate increased willingness to exercise writ jurisdiction in genuine cases, particularly where systemic failures or administrative lapses have prevented timely compliance.

Key Takeaways and Best Practices

Essential Compliance Guidelines

Proactive Timeline Management: Maintain detailed compliance calendars marking all critical dates, including appeal filing deadlines and condonation application periods. Implement automated reminder systems to avoid inadvertent delays.

Documentation Excellence: Establish robust documentation systems ensuring all supporting evidence is contemporaneous, properly authenticated, and comprehensively indexed. Quality documentation significantly enhances condonation prospects.

Professional Engagement: Engage qualified GST professionals early in the dispute resolution process. Expert guidance becomes crucial for evaluating condonation prospects and presenting compelling cases to appellate authorities.

Strategic Considerations

Cost-Benefit Analysis: Evaluate the financial implications of delayed appeals, including pre-deposit requirements, professional fees, and potential adverse outcomes. Sometimes accepting adverse orders may be more economical than prolonged litigation.

Alternative Remedies: Consider parallel remedies such as rectification applications under Section 161, revision petitions, or settlement mechanisms before pursuing condonation routes.

Risk Assessment: Assess the strength of your case on merits alongside condonation prospects. Strong cases on merit often receive favorable consideration even with marginal condonation grounds.

Final Thoughts

The GST appeal condonation of delay mechanism represents a critical balance between administrative efficiency and taxpayer rights in India’s evolving tax landscape. Through comprehensive analysis of legal provisions, judicial precedents, and practical implementation challenges, this guide demonstrates that successful condonation requires meticulous preparation, strong legal grounds, and thorough documentation.

The recent amendments have significantly enhanced the digital infrastructure and procedural clarity, making the condonation process more transparent and accessible to taxpayers. However, the fundamental requirement of demonstrating sufficient cause remains unchanged, requiring taxpayers to present compelling evidence of circumstances beyond their control.

Key takeaways from this comprehensive analysis include the importance of understanding the strict 120-day outer limit, the critical role of proper documentation, and the evolving judicial approach toward liberal interpretation of sufficient cause. The recent High Court decisions provide valuable guidance on presenting condonation applications effectively and understanding the scope of judicial relief available.

For taxpayers navigating the complex terrain of GST appeals and condonation procedures, professional guidance becomes indispensable. The interplay between statutory provisions, judicial interpretations, and administrative practices requires specialized expertise to ensure optimal outcomes.

Moving forward, taxpayers should focus on proactive compliance strategies, robust documentation systems, and continuous monitoring of legal developments. The GST appeal condonation framework will continue evolving, and staying informed about these changes will be crucial for effective tax compliance and dispute resolution.

For comprehensive GST compliance solutions and expert guidance follow TaxGroww.