Table of Contents

Introduction

The introduction of the Goods and Services Tax (GST) in July 2017 marked a significant transformation in India’s indirect tax structure. Among the various compliance mechanisms introduced under this regime, the electronic Way Bill (e-Way Bill) stands as a crucial instrument to track the movement of goods and prevent tax evasion. This digital document has replaced the traditional way bill system that existed under the previous tax regime, bringing transparency and efficiency to the logistics and supply chain ecosystem.

Before diving into the intricacies of the e-Way Bill system, it’s important to understand its foundational purpose. The e-Way Bill serves as an electronic document generated on the GST portal that provides detailed information about the movement of goods from one place to another. It acts as a digital trail for tax authorities to verify that goods being transported have undergone proper tax compliance.

The need for such a system arose from the challenges faced during the pre-GST era, where each state had its own way bill requirements, leading to delays at check posts and increasing the cost of doing business. The e-Way Bill system aims to create a unified, corruption-free mechanism that facilitates seamless interstate and intrastate movement of goods while ensuring tax compliance.

This article provides an in-depth analysis of the e-Way Bill system under GST, covering its legal framework, operational aspects, recent amendments, and practical considerations for businesses. Whether you’re a small business owner, a tax professional, or a logistics manager, understanding the nuances of the e-Way Bill system is essential for ensuring compliance and avoiding penalties.

Legal Framework of e-Way Bill

Statutory Provisions

The electronic Way Bill system derives its legal basis from Section 68 of the Central Goods and Services Tax (CGST) Act, 2017. This section empowers the government to mandate that the person in charge of a conveyance carrying goods of consignment value exceeding specified limits must carry prescribed documents and devices. Building upon this foundation, Rule 138 of the CGST Rules, 2017 elaborates on the e-Way Bill system, specifying the conditions, processes, and requirements for its generation and validation.

The e-Way Bill rules were initially notified vide Notification No. 27/2017 – Central Tax dated 30th August 2017. However, due to technical challenges and implementation issues, the nationwide rollout was postponed. Eventually, the interstate e-Way Bill system was implemented from April 1, 2018, while the intrastate system was rolled out in a phased manner across different states.

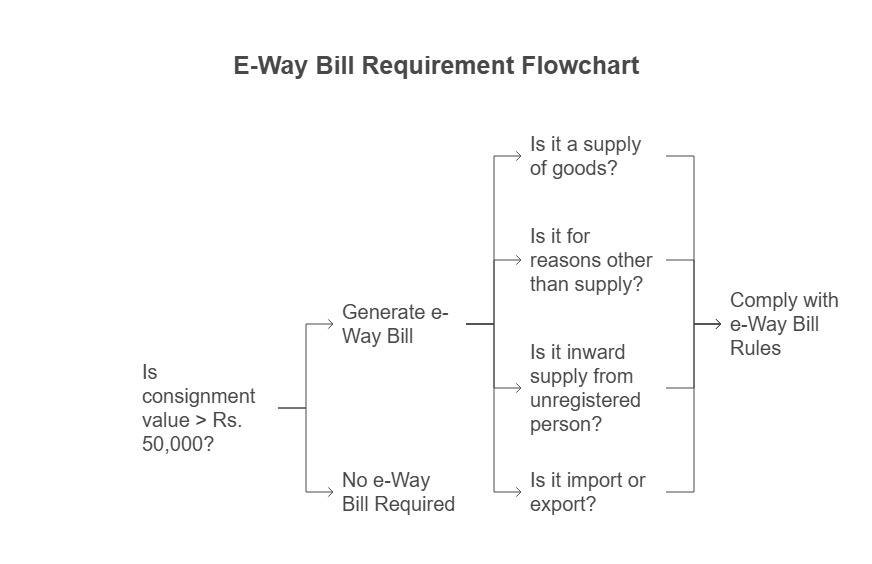

Applicability and Threshold Limits

Understanding when an e-Way Bill is required is fundamental to compliance. According to Rule 138(1) of the CGST Rules, every registered person who causes movement of goods with consignment value exceeding Rs. 50,000 must generate an e-Way Bill. This applies to:

- Supply of goods: When goods are supplied by a registered person, either as sale, transfer, barter, or exchange

- Reasons other than supply: Includes goods sent for job work, exhibition, or approval basis

- Inward supply from unregistered person: When a registered person receives goods from an unregistered supplier

- Import and export: For goods being imported into or exported from India

The threshold limit of Rs. 50,000 refers to the value of goods being transported, including the tax component. It’s worth noting that this limit applies per consignment per conveyance, not the aggregate value of all goods being transported in a vehicle.

Certain exceptions to this threshold have been provided by the government:

- Inter-state transfer of handicraft goods by exempt craftsmen

- Movement of goods like used personal and household effects

- Transport of certain specified goods as notified by the government

The Commissioner, through notification, may also exempt certain goods from the requirement of e-Way Bill generation, either generally or subject to specific conditions.

What is an e-Way Bill?

Definition and Purpose

An e-Way Bill (electronic Way Bill) is a unique document generated electronically on the GST portal that must accompany the physical movement of goods valued above Rs. 50,000. It serves as digital evidence that the goods being transported have undergone proper tax compliance.

The primary purposes of the e-Way Bill system are:

- Track movement of goods: To monitor the interstate and intrastate movement of goods for preventing tax evasion

- Eliminate state barriers: To ensure smooth movement of goods across state borders by removing check posts

- Reduce logistics costs: To decrease the time spent at state borders for documentation verification

- Prevent tax evasion: To curb underreporting and tax evasion through digital tracking

- Create a unified national market: To facilitate seamless movement of goods across the country

The e-Way Bill contains critical information about the goods being transported, the consignor, consignee, transporter, and the vehicle carrying the goods. This digital document must be generated before the commencement of movement of goods and can be produced electronically or as a print-out to the tax authorities when requested.

Types of e-Way Bills

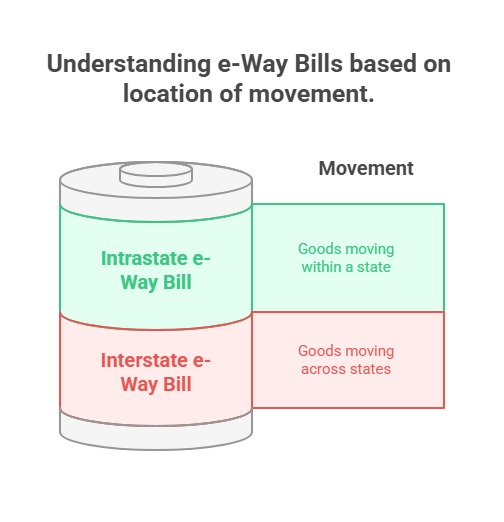

The e-Way Bill system primarily recognizes two types of e-Way Bills based on the nature of movement:

- Interstate e-Way Bill: Generated when goods move from one state to another. The format and requirements for these bills are uniform across the country as they fall under the central jurisdiction.

- Intrastate e-Way Bill: Generated when goods move within the same state. While the central government has prescribed the basic framework, states have been given some flexibility in implementing specific requirements.

Additionally, e-Way Bills can be categorized based on the mode of transport:

- Regular e-Way Bill: Generated for road transport where vehicle details are known at the time of generation.

- Bill-to-Ship-to e-Way Bill: Used in scenarios where goods are billed to one party but shipped to another party.

- Multi-vehicle e-Way Bill: Used when goods need to be transferred from one vehicle to another during transit.

- Over-Dimensional Cargo e-Way Bill: Special provisions apply for oversized cargo that requires specialized vehicles.

Each type serves specific business scenarios and has its own set of operational nuances that businesses need to understand for proper compliance.

Who Needs to Generate an e-Way Bill?

The responsibility for generating an e-Way Bill varies depending on the nature of the transaction and the parties involved. According to Rule 138(1) of the CGST Rules, the following persons are responsible for e-Way Bill generation:

For Regular Supply Transactions

- When the supplier is registered: The registered supplier or the recipient (if authorized by the supplier) must generate the e-Way Bill.

- When the recipient is unregistered: The registered supplier must generate the e-Way Bill.

- When the supplier is unregistered and recipient is registered: The registered recipient must generate the e-Way Bill under reverse charge mechanism as per Section 9(4) of the CGST Act.

- When both supplier and recipient are unregistered: No e-Way Bill is required as unregistered persons are not covered under GST, unless the value exceeds Rs. 50,000 and transportation is by a registered transporter.

For Special Scenarios

- Job work: When goods are sent for job work, the principal manufacturer or the job worker can generate the e-Way Bill.

- Transporter responsibility: If the consignor or consignee hasn’t generated the e-Way Bill and the value exceeds Rs. 50,000, the transporter must generate it based on the tax invoice or delivery challan provided.

- Imports: In case of imports, the importer or the recipient must generate the e-Way Bill.

- Exhibition or approval basis: When goods are sent on approval basis, the registered person causing the movement must generate the e-Way Bill.

The failure to generate an e-Way Bill when required can result in penalties and detention of goods. Section 129 of the CGST Act provides for the detention, seizure, and release of goods and conveyances in transit if they are transported without a valid e-Way Bill.

How to Generate an e-Way Bill?

The process of generating an e-Way Bill involves several steps and can be done through multiple channels. Here’s a comprehensive guide on how to generate an e-Way Bill:

Registration and Prerequisites

Before generating an e-Way Bill, businesses must complete these prerequisites:

- GST Registration: The business must be registered under GST and have a valid GSTIN.

- e-Way Bill Registration: Even with a GSTIN, separate registration on the e-Way Bill portal (https://ewaybillgst.gov.in) is required.

- Username and Password: During registration, credentials are created for accessing the portal.

- Required Documents: Tax invoice, bill of supply, delivery challan, or bill of entry for imports should be readily available as they contain information needed for the e-Way Bill.

Methods of Generation

The e-Way Bill can be generated through various methods:

- Web Portal: The official e-Way Bill portal allows direct generation through a web interface.

- SMS Facility: For businesses with limited internet access, e-Way Bills can be generated via SMS.

- Mobile Application: The official e-Way Bill app facilitates on-the-go generation.

- API Integration: Large businesses can integrate their ERP systems with the e-Way Bill system through APIs.

- Through GST Suvidha Providers (GSPs): Authorized service providers can generate e-Way Bills on behalf of taxpayers.

Step-by-Step Process

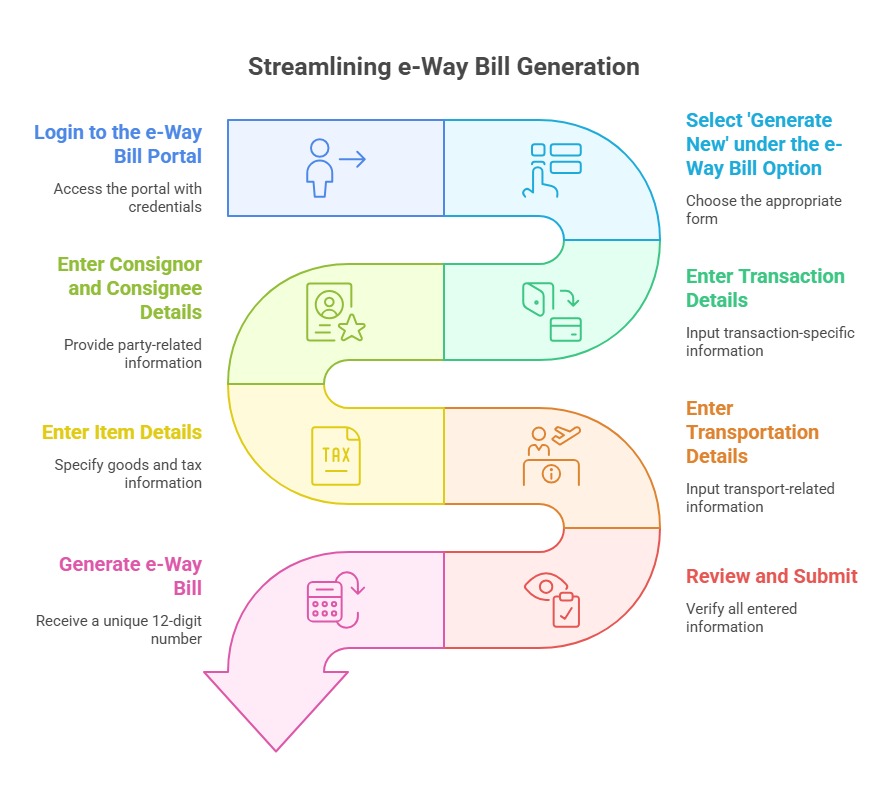

- Login to the e-Way Bill Portal: Enter the username and password to access the portal.

- Select ‘Generate New’ under the e-Way Bill Option: Choose the appropriate form based on the transaction type.

- Enter Transaction Details:

- Transaction type (outward supply, inward supply, etc.)

- Sub-type (supply, export/import, job work, etc.)

- Document details (invoice number, date, etc.)

- Enter Consignor and Consignee Details:

- Names, GSTINs, and addresses of both parties

- Place of dispatch and delivery

- Enter Item Details:

- HSN code of the goods

- Description of goods

- Quantity and taxable value

- Tax rates (CGST, SGST, IGST, Cess)

- Enter Transportation Details:

- Mode of transport (road, rail, air, ship)

- Distance in kilometers

- Vehicle number (for road transport)

- Transporter ID and name

- Review and Submit: Verify all entered information for accuracy.

- Generate e-Way Bill: Upon submission, a unique 12-digit e-Way Bill number is generated.

Special Scenarios

- Bill-to-Ship-to Transactions: When billing and shipping addresses differ, specific fields in the form need to be filled accordingly.

- Multi-modal Transportation: When goods change vehicles during transit, the transporter can update vehicle details without generating a new e-Way Bill.

- Bulk Generation: For businesses with multiple consignments, bulk generation facility is available where multiple e-Way Bills can be generated simultaneously using Excel uploads.

- JSON/XML Upload: Technical users can prepare JSON/XML files as per the prescribed format and upload them for batch processing.

The generated e-Way Bill can be printed, emailed, or SMS-ed to relevant parties. It’s mandatory to carry either a physical copy or the electronic version during transportation.

Validity Period of e-Way Bills

The validity of an e-Way Bill is a critical aspect of compliance, as transporting goods with an expired e-Way Bill is treated the same as transporting without one. The validity period is determined based on the distance the goods need to travel.

Distance-Based Validity

Rule 138(10) of the CGST Rules prescribes the following validity periods:

Distance | Validity Period |

Up to 100 km | 1 day from the time of generation |

For every additional 100 km or part thereof | +1 additional day |

Over dimensional cargo (for every 20 km) | 1 day |

The distance is calculated from the place of business of the consignor to the place of delivery specified in the e-Way Bill.

Special Provisions for Validity

- Calculation of Validity Period: The validity period starts from the time of generation of the e-Way Bill, not from the time of commencement of movement.

- Over Dimensional Cargo: For cargo that exceeds the standard dimensions permitted for transport vehicles, the validity is calculated as one day for every 20 kilometers.

- Extension of Validity: In exceptional circumstances, such as natural calamities, law and order issues, or vehicle breakdown, the Commissioner may extend the validity period.

- Multiple trips on Single e-Way Bill: For specific industries like oil and gas where multiple trips are made using the same delivery challan, special provisions allow multiple trips within the validity period.

Extension of e-Way Bill Validity

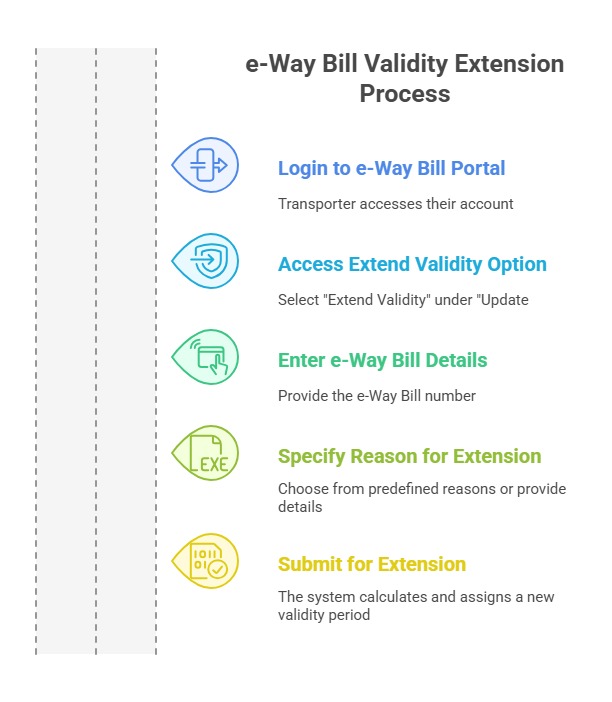

If the goods cannot be transported within the validity period due to exceptional circumstances, the transporter can extend the validity period. The process involves:

- Login to e-Way Bill Portal: The transporter must access their account.

- Access the Extend Validity Option: Under the “Update” section, select “Extend Validity.”

- Enter e-Way Bill Details: Provide the e-Way Bill number that needs extension.

- Specify Reason for Extension: Choose from predefined reasons or provide specific details.

- Submit for Extension: The system will calculate and assign a new validity period.

It’s important to note that the extension must be requested before the expiry of the original validity period. Once an e-Way Bill expires, a new one must be generated for the continued movement of goods.

Practical Considerations

- Transit Storage: If goods need to be stored during transit, the validity period continues to run, which needs to be factored into transportation planning.

- Vehicle Breakdown: In case of vehicle breakdown, the transporter should update the vehicle details and may need to request validity extension.

- Multiple Consignments in One Vehicle: Each consignment requires a separate e-Way Bill with its own validity period, even if transported in the same vehicle.

- Trans-shipment: When goods are transferred from one vehicle to another, the validity period doesn’t reset but continues from the original date and time of generation.

Understanding and adhering to these validity provisions is crucial to avoid penalties and ensure smooth movement of goods.

Updating and Cancellation of e-Way Bills

The e-Way Bill system provides flexibility to update information or cancel incorrectly generated e-Way Bills under specific circumstances. Understanding these provisions is essential for businesses to manage logistics efficiently.

Updating e-Way Bill Information

Once generated, certain fields of an e-Way Bill can be updated while others remain fixed:

Fields that can be updated:

- Vehicle Number: When goods are transferred from one vehicle to another.

- Transporter Details: When the responsibility for transportation changes.

- Reason for Transportation: If the purpose of movement changes.

- Place of Delivery: Limited modifications may be allowed within the same destination state.

Fields that cannot be updated:

- Consignor and Consignee details

- HSN Codes and description of goods

- Value of goods and tax amounts

- Document number (Invoice/Challan)

The process for updating involves:

- Login to the e-Way Bill portal

- Select ‘Update Vehicle No.’ under the ‘Update’ option

- Enter the e-Way Bill number to be updated

- Enter new vehicle or transporter details

- Provide reasons for the change

- Submit the update

According to Rule 138(5A), the consignor, consignee, or transporter can assign the e-Way Bill to another registered transporter for further movement of goods.

Cancellation of e-Way Bills

Rule 138(9) of the CGST Rules provides for cancellation of e-Way Bills under the following conditions:

- Time Constraint: An e-Way Bill can be cancelled within 24 hours of generation.

- Non-movement of Goods: Cancellation is allowed only if the goods have not moved as per the details furnished.

- Duplicate Generation: If multiple e-Way Bills were generated for the same consignment.

The cancellation process involves:

- Login to the e-Way Bill portal

- Select ‘Cancel’ under the ‘e-Way Bill’ option

- Enter the e-Way Bill number to be cancelled

- Specify the reason for cancellation

- Submit the cancellation request

It’s important to note that once goods have moved, the e-Way Bill cannot be legally cancelled. Any attempt to do so may attract penalties under Section 122 of the CGST Act for providing false information.

Practical Scenarios

- Rejection of Goods by Recipient: If goods are rejected at the delivery point, the return movement requires a new e-Way Bill; the original cannot be reused.

- Partial Movement of Goods: If only part of the consignment is transported, the original e-Way Bill can be used, but the actual quantity moved should be updated.

- Trans-shipment: When goods are moved to another vehicle due to breakdown or other reasons, only the vehicle details need to be updated without cancelling the original e-Way Bill.

- Return of Goods: If goods need to be returned after delivery, a fresh e-Way Bill needs to be generated for the return journey.

Proper management of e-Way Bill updates and cancellations helps businesses avoid unnecessary complications with tax authorities and ensures smooth logistics operations.

Verification and Enforcement

The e-Way Bill system includes robust verification and enforcement mechanisms to ensure compliance. Understanding these aspects is crucial for businesses to avoid detention of goods and penalties.

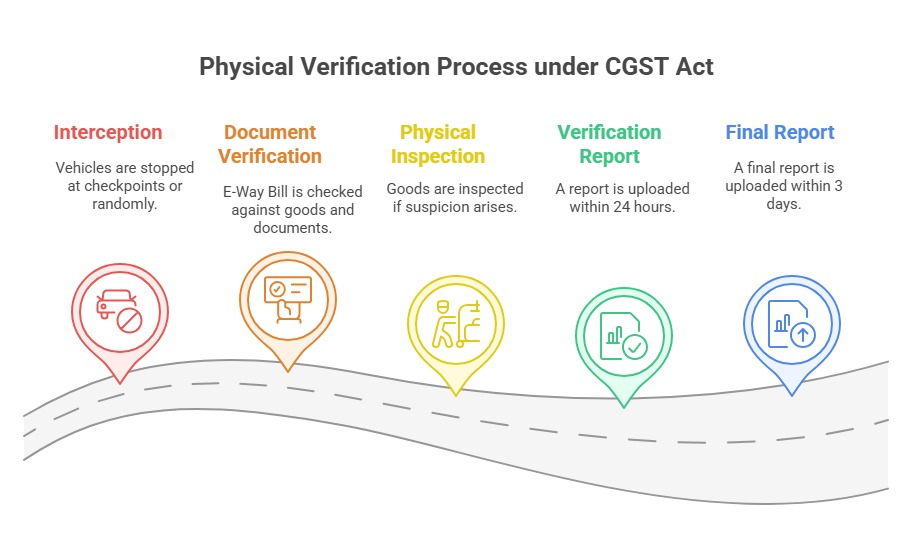

Physical Verification Process

Under Section 68 of the CGST Act, any person in charge of a conveyance carrying goods may be required to stop the vehicle and allow inspection of goods and verification of documents by tax authorities. The verification process typically involves:

- Interception: Vehicles may be intercepted at designated checkpoints or randomly by mobile squads.

- Document Verification: The officer verifies the e-Way Bill against:

- Physical goods being transported

- Tax invoice or delivery challan

- Vehicle registration documents

- Physical Inspection: In case of suspicion, goods may be physically inspected to confirm quantities and descriptions.

- Verification Report: The officer must upload a verification report within 24 hours of inspection on the portal as per Form GST EWB-03.

- Final Report: A final report must be uploaded within 3 days of inspection.

As per Circular No. 41/15/2018-GST dated April 13, 2018, physical verification of a particular conveyance should not be carried out more than once during the journey, except in case of specific intelligence about tax evasion.

Detention and Seizure Procedures

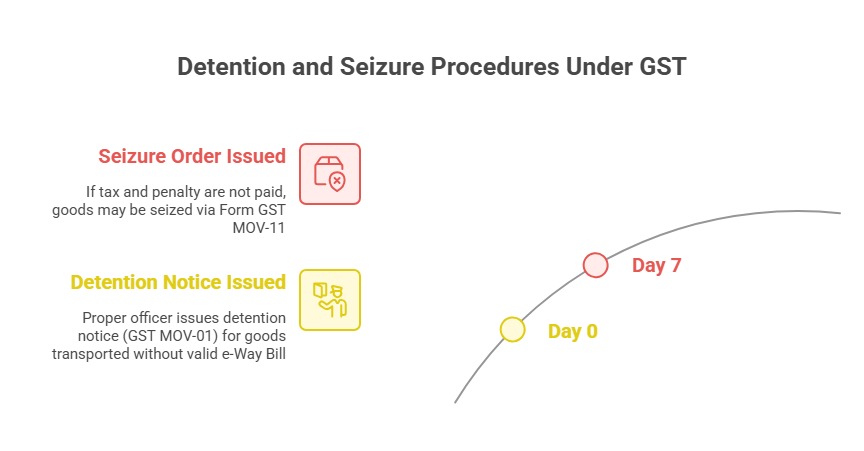

If goods are transported without a valid e-Way Bill or with discrepancies, the following actions may be taken as per Section 129 of the CGST Act:

- Detention Notice: The proper officer issues a detention notice in Form GST MOV-01.

- Release Options:

- For taxable goods: Payment of applicable tax and penalty equal to 100% of the tax payable

- For exempt goods: Payment of penalty of 2% of the value of goods or Rs. 25,000, whichever is less

- Seizure Order: If tax and penalty are not paid within 7 days, the goods may be seized via Form GST MOV-11.

- Appeal Process: The person can file an appeal against detention or seizure under Section 107 of the CGST Act.

Penalties for Non-compliance

The consequences of non-compliance with e-Way Bill provisions are significant:

- Section 122(1)(xiv): A penalty of Rs. 10,000 or the tax sought to be evaded, whichever is higher, for transporting goods without an e-Way Bill.

- Section 129(3): For transporters, a penalty of Rs. 10,000 or the tax payable on such goods, whichever is higher.

- Confiscation of Goods: In extreme cases, goods may be confiscated under Section 130 of the CGST Act.

- Vehicle Detention: The vehicle carrying goods without proper documentation may be detained until penalties are paid.

Electronic Verification System

To modernize enforcement, many states have implemented:

- RFID-based Verification: RFID sensors at checkpoints scan vehicles and automatically verify e-Way Bills.

- Data Analytics: The GST system uses analytics to identify suspicious patterns and potential tax evasion.

- Risk Parameters: High-risk consignments are flagged for physical verification based on predefined parameters.

- Integration with Fastag: Some states have integrated e-Way Bill verification with the national electronic toll collection system.

The verification and enforcement system aims to balance the need for compliance with facilitating ease of doing business. However, businesses should ensure strict adherence to e-Way Bill provisions to avoid disruptions in their supply chain.

Special Cases and Exemptions

The e-Way Bill system, while comprehensive, recognizes that certain goods or movements require special treatment. Various exemptions and special provisions have been introduced to address specific business needs while maintaining the integrity of the tracking system.

Exempt Categories of Goods

As per Notification No. 74/2018-Central Tax dated 31st December 2018, the following categories of goods are exempt from e-Way Bill requirements regardless of value:

- Agricultural Products: Fresh fruits, vegetables, milk, curd, lassi, buttermilk, and related perishable items.

- Non-GST Goods: Alcoholic liquor for human consumption, petroleum crude, high-speed diesel, motor spirit (petrol), natural gas, and aviation turbine fuel.

- Essential Commodities: Specified goods like newspaper, salt, food grains, flour, sugar, and unprocessed tea.

- Medical Supplies: Life-saving drugs, medical oxygen, and related medical equipment.

- Defense Materials: Goods being transported under Ministry of Defense as consignor.

- Household Effects: Used personal and household effects during residential shifting.

- Empty Cargo Containers: Being returned to their place of origin.

- Relief Materials: Goods being transported for relief in cases of natural disasters, calamities, or emergencies.

The above exemptions are provided to ensure essential services and goods movement aren’t hindered by compliance requirements.

Special Provisions for Specific Industries

Certain industries have unique operational requirements, leading to special provisions:

- Jewelry Transport: For movement of gold, silver, precious stones, and jewelry (Chapter 71, excluding HSN 7117):

- Interstate Movement: An e-Way Bill is not required, regardless of the consignment value. This special exemption recognizes the security concerns and unique nature of precious metals transportation.

- Intrastate Movement: Requirements depend on state-specific notifications. Some states mandate an e-Way Bill for consignment values exceeding ₹2 lakh. For instance, Kerala requires an e-Way Bill for gold consignments above ₹2 lakh.

- This special treatment acknowledges both the high value and security concerns associated with jewelry transport.

Imitation Jewelry (HSN 7117):

- Interstate and Intrastate Movement: An e-Way Bill is mandatory if the consignment value exceeds ₹50,000. This category does not benefit from the exemptions applicable to precious jewelry.

- Standard e-Way Bill rules apply as imitation jewelry is not classified under the special category of precious metals and stones.

- Courier Services: Special provisions under the E-Way Bill system permit courier agencies and logistics operators to generate a Consolidated E-Way Bill (Form GST EWB-02) by clubbing multiple individual consignments. If the value of each individual parcel does not exceed ₹50,000, generation of an individual E-Way Bill is not mandatory unless mandated by the transporter under Rule 138(7) or by state-specific notifications. However, if even a single consignment exceeds ₹50,000, a separate E-Way Bill must be generated.

- Oil and Gas Sector: For continuous supply operations such as transfer of petroleum and gas products through pipelines or similar networks, special provisions exist under Rule 55(5). Movement of goods via pipelines may use a Delivery Challan instead of a tax invoice. Additionally, products such as HSD, petrol, crude oil, ATF, and natural gas are currently not subject to GST, and hence are exempted from E-Way Bill requirements as per Notification No. 12/2018 – Central Tax. For taxable petroleum products like lubricants, E-Way Bills are applicable. Extended validity of E-Way Bills applies for long-distance movement as per standard rules.

- Exhibition and Events: Goods transported for display or exhibition purposes (not involving supply) are required to be moved under a Delivery Challan in place of a tax invoice. Where the value of goods exceeds ₹50,000, an E-Way Bill must be generated even though the goods are not being sold. Upon return, a separate E-Way Bill with a new Delivery Challan must be generated. In case of multiple consignments, a Consolidated E-Way Bill may be generated by the transporter.

- E-commerce Operations: E-Commerce operators and their logistics partners handling multiple consignments are permitted to generate Consolidated E-Way Bills for the transportation of goods. Individual E-Way Bills are mandatory for each consignment where the invoice value exceeds ₹50,000. If goods are transported through unregistered transporters, a unique Transporter ID (TRANSIN) may be used to generate E-Way Bills. Sellers on e-commerce platforms must ensure compliance with E-Way Bill rules before dispatch.

Zero-Value Transactions

Certain movements involve goods without commercial value but still require documentation:

- Job Work: When goods are sent for job work without transfer of ownership, e-Way Bills are required even if the commercial value is zero.

- Warranty Replacements: Parts being replaced under warranty may not have commercial value but require e-Way Bills.

- Free Samples: Though distributed without charge, samples exceeding Rs. 50,000 in value require e-Way Bills.

- Inter-branch Transfers: Movement of goods between different branches of the same legal entity requires e-Way Bills even without sale consideration.

For such zero-value transactions, the value to be declared is the transaction value as per Section 15 of the CGST Act, which may be the value of similar goods or cost of production.

Special Economic Zones and Export Import

Special provisions apply for SEZ operations and international trade:

- SEZ to DTA (Domestic Tariff Area): Movement requires e-Way Bills with special coding to identify SEZ transactions.

- Imports: For imported goods, e-Way Bills must be generated based on the bill of entry once goods are cleared from customs and before transportation within the country.

- Exports: For export goods, e-Way Bills must accompany goods until they reach the port, airport, or land customs station.

These special cases and exemptions demonstrate the system’s adaptability while maintaining its core purpose of tracking goods movement for tax compliance.

Recent Amendments and Notifications

The e-Way Bill system has evolved since its inception through various amendments and notifications to address implementation challenges and improve user experience. Staying updated with these changes is essential for businesses to ensure compliance.

Key Amendments in 2023-24

- Notification No. 11/2023-Central Tax dated 31st March 2023:

- Extended the validity period for e-Way Bills generated for Over Dimensional Cargo from 1 day per 20 km to 1 day per 40 km

- This change was introduced to address logistical challenges faced by transporters of oversized cargo

- Notification No. 18/2023-Central Tax dated 1st August 2023:

- Increased the threshold limit for mandatory e-Way Bill generation for intra-state movement in specific states from Rs. 50,000 to Rs. 1,00,000

- States covered: Delhi, Gujarat, Haryana, Punjab, Rajasthan, and Uttar Pradesh

- This measure was introduced to reduce compliance burden for small businesses

- Circular No. 187/19/2023-GST dated 19th September 2023:

- Clarified that for multimodal transport, the e-Way Bill validity should be calculated based on the distance covered in each mode of transport

- Provided guidelines for handling transit storage during multimodal transportation

- Notification No. 27/2023-Central Tax dated 15th December 2023:

- Introduced provision for automatic extension of e-Way Bill validity in case of vehicle breakdown or natural calamities

- Implemented self-declaration mechanism for such extensions with post-verification by tax authorities

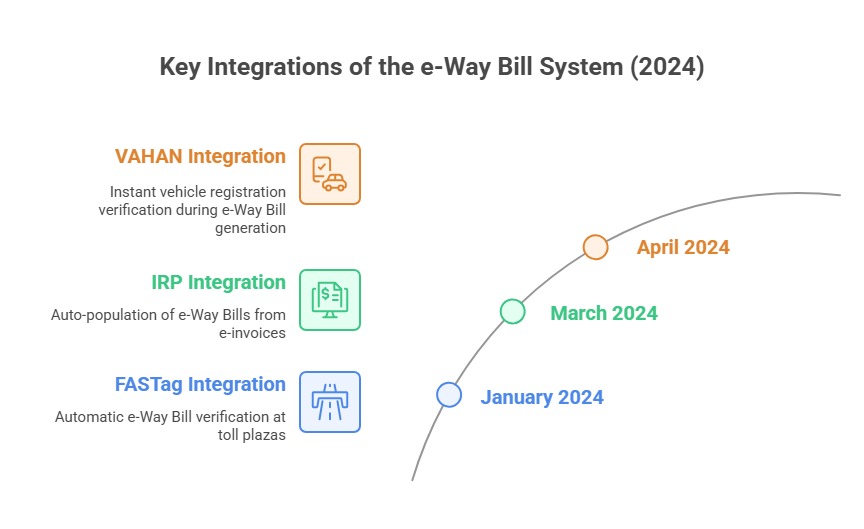

Integration with Other Systems

Recent technological enhancements have focused on integrating the e-Way Bill system with other digital platforms:

- Fastag Integration (January 2024):

- The e-Way Bill system has been integrated with the National Electronic Toll Collection (FASTag) system

- This integration enables automatic verification of e-Way Bills at toll plazas

- Helps identify discrepancies between declared and actual movement of goods

- GST Invoice Registration Portal (IRP) Integration (March 2024):

- Auto-population of e-Way Bill forms from e-invoices generated on the Invoice Registration Portal

- Eliminates duplicate data entry and reduces errors

- Applicable for businesses with turnover exceeding Rs. 5 crore

- VAHAN Database Integration (April 2024):

- Integration with the national vehicle database for instant verification of vehicle registration details

- Automatic validation of vehicle ownership and capacity details during e-Way Bill generation

Relaxations During COVID-19 and Their Current Status

During the COVID-19 pandemic, several relaxations were provided for e-Way Bill compliance, many of which have since been withdrawn:

- Extended Validity Period: The validity period of e-Way Bills was extended during lockdown periods. This relaxation has been withdrawn as of June 2023.

- Blanket Extension: Special provisions for blanket extension of e-Way Bills expiring between March 20, 2020, and April 15, 2020. This was a one-time measure no longer in effect.

- Reduced Physical Verification: Instructions to minimize physical verification of vehicles. Normal verification procedures have been restored since January 2023.

Future Roadmap (Announced Initiatives)

Based on official announcements, the following enhancements are expected in the near future:

- AI-Based Risk Assessment (Expected Q3 2024):

- Implementation of artificial intelligence for identifying high-risk consignments

- Dynamic parameter-based verification to reduce unnecessary stoppages of vehicles

- QR Code Based Verification (Expected Q4 2024):

- Introduction of QR codes on e-Way Bills for instant verification

- Mobile app for officers to scan and verify details on the spot

- Expansion of Auto Calculation Features (Expected Q1 2025):

- Enhancement of the system to automatically calculate distances for validity

- Integration with mapping services for accurate distance calculations

Businesses should stay vigilant about these upcoming changes and prepare their systems and processes accordingly to ensure seamless compliance with e-Way Bill requirements.

Common Challenges and Solutions

Despite its digital nature, the e-Way Bill system presents various challenges to businesses. Understanding these challenges and their practical solutions can help ensure smooth compliance and avoid penalties.

Technical Challenges

- Portal Downtime and Slowness

- Challenge: The e-Way Bill portal occasionally experiences slowdowns during peak filing periods, causing delays in generation.

- Solution: Prepare and generate e-Way Bills well in advance of transportation. Utilize the bulk generation facility during off-peak hours (early morning or late evening). Keep alternative methods like SMS generation ready as backup.

- Data Integration Issues

- Challenge: Discrepancies between ERP data and e-Way Bill portal requirements cause validation errors.

- Solution: Implement middleware solutions that format data correctly before transmission. Regularly update master data in ERP systems to match GST portal formats. Conduct periodic reconciliation of data between systems.

- API Connectivity Problems

- Challenge: Businesses using API integration face connectivity and authentication issues.

Solution: Implement proper error handling and retry mechanisms in API integration. Maintain backup connectivity options. Keep API credentials secure and updated periodically.

Operational Challenges

- Last-Minute Transportation Changes

- Challenge: Vehicle breakdowns or last-minute logistics changes require quick updates to e-Way Bills.

- Solution: Train multiple team members on e-Way Bill updating procedures. Implement mobile-based solutions for on-the-go updates. Establish clear communication protocols between drivers, transporters, and the e-Way Bill team.

- Multi-modal Transportation

- Challenge: Managing e-Way Bills when goods change transportation modes (road to rail to ship).

- Solution: Plan the entire journey in advance and document transfer points. Update vehicle/mode details promptly at each transfer point. Consider using GSP services that specialize in multi-modal transport documentation.

- Managing Consolidated Shipments

- Challenge: Handling multiple small consignments in a single vehicle, each requiring separate e-Way Bills.

- Solution: Utilize the bulk generation facility for multiple consignments. Implement barcode/QR code systems to track individual packages within consolidated shipments. Consider transportation management systems that handle consolidated e-Way Bills.

Compliance Challenges

- Validity Expiration During Transit

- Challenge: e-Way Bills expiring before goods reach their destination due to unforeseen delays.

- Solution: Calculate validity periods conservatively, accounting for potential delays. Monitor approaching expiry dates and extend validity where permitted. Train drivers to notify dispatchers about potential delays early.

- Interstate Variations in Requirements

- Challenge: Different states might have additional requirements beyond the central e-Way Bill system.

- Solution: Maintain a state-wise compliance checklist and update it regularly. Consider region-specific training for logistics teams. Engage with local tax consultants for specific interstate movements.

- HSN Code and Value Discrepancies

- Challenge: Incorrect HSN codes or valuation discrepancies leading to detention of goods.

- Solution: Implement master data validation for HSN codes. Conduct periodic internal audits of e-Way Bill data against invoices. Develop clear guidelines for valuation of different types of movements (samples, repairs, returns, etc.).

Best Practices to Overcome Challenges

- Robust Documentation System

- Maintain digital copies of all e-Way Bills with supporting documents

- Implement version control for updated e-Way Bills

- Create audit trails for all changes made to e-Way Bills

- Team Training and SOPs

- Conduct regular training sessions for staff handling e-Way Bills

- Develop step-by-step SOPs for routine and contingency scenarios

- Create troubleshooting guides for common errors

- Technology Adoption

- Implement e-Way Bill management software that integrates with ERP systems

- Consider mobile applications for drivers to carry digital copies

- Use analytics to identify patterns in transportation and optimize routes within validity periods

- Preventive Compliance Measures

- Conduct periodic reconciliation of e-Way Bill data with GSTR-1 returns

- Implement pre-dispatch checks for all consignments requiring e-Way Bills

- Maintain communication channels with local GST authorities for clarifications

By addressing these challenges proactively, businesses can minimize disruptions in their supply chain and ensure smooth compliance with e-Way Bill requirements.

Conclusion

The e-Way Bill system represents a significant technological advancement in India’s tax administration landscape. It has successfully transformed the traditional way of monitoring goods movement into a digital, transparent, and efficient process. Since its nationwide implementation in April 2018, the system has helped reduce tax evasion, minimize transit delays, and create a unified national market for the movement of goods across the country.

Key Takeaways

- Compliance is Non-negotiable: With stringent penalties for non-compliance, businesses must ensure meticulous adherence to e-Way Bill provisions. The cost of non-compliance far exceeds the effort required for proper documentation and can result in significant financial and operational setbacks.

- Technological Integration is Essential: As the system evolves, businesses that integrate the e-Way Bill system with their ERP and logistics management will gain significant operational advantages. Such integration reduces manual effort, minimizes errors, and ensures real-time compliance with changing regulations.

- Preparation Beats Reaction: Proactive planning for e-Way Bill generation and management is far more effective than reactive approaches. Establishing clear SOPs, training multiple team members, and preparing for contingencies ensures business continuity even during technical glitches or enforcement checks.

- Documentation is Critical: Maintaining comprehensive records of all e-Way Bills, underlying invoices, and delivery challans is essential for addressing any queries from tax authorities. Digital document management systems can significantly ease this compliance burden and provide an audit trail when needed.

- Continuous Monitoring is Necessary: The e-Way Bill system continues to evolve through notifications, circulars, and amendments. Businesses must stay updated and adjust their processes accordingly to remain compliant and avoid unnecessary complications.

The e-Way Bill system exemplifies how digital initiatives can transform regulatory compliance while benefiting both the government and businesses. By reducing physical check posts, eliminating paperwork, and streamlining verification processes, it has contributed significantly to ease of doing business in India and reduced logistics costs across the supply chain.

For businesses operating in this dynamic tax environment, embracing the e-Way Bill system not just as a compliance requirement but as an opportunity to digitize and streamline their logistics operations will yield long-term benefits in efficiency, transparency, and cost reduction. The system continues to evolve, and staying updated with the latest developments is crucial.

To stay informed about the latest updates, amendments, and practical guidance on e-Way Bill compliance and other GST matters, follow TaxGroww for regular, reliable, and professional updates on GST regulations. Our expert insights and timely notifications can help businesses navigate the complexities of GST compliance with confidence and precision.

References and Resources

For readers seeking additional information or clarification on e-Way Bill provisions, the following official resources and references can be consulted:

Official Resources

- e-Way Bill Portal: https://ewaybillgst.gov.in

- The official portal for e-Way Bill generation, updates, and cancellations

- Contains user manuals, FAQs, and help videos

- Central Board of Indirect Taxes and Customs (CBIC): https://cbic-gst.gov.in

- Official website for all GST-related notifications, circulars, and clarifications

- Repository of GST Acts, Rules, and notifications

- GST Council: https://gstcouncil.gov.in

- Minutes of GST Council meetings discussing e-Way Bill provisions

- Policy decisions and recommendations regarding the e-Way Bill system

Legal References

- Central Goods and Services Tax Act, 2017

- Section 68: Inspection of goods in movement

- Section 129: Detention, seizure, and release of goods and conveyances in transit

- Section 130: Confiscation of goods or conveyances and levy of penalty

- Central Goods and Services Tax Rules, 2017

- Rule 138: Information to be furnished prior to commencement of movement of goods and generation of e-Way Bill

- Rule 138A: Documents and devices to be carried by a person-in-charge of a conveyance

- Rule 138B: Verification of documents and conveyances

- Rule 138C: Inspection and verification of goods

- Rule 138D: Facility for uploading information regarding detention of vehicle

- Key Notifications

- Notification No. 27/2017-Central Tax dated 30.08.2017: Initial notification of e-Way Bill Rules

- Notification No. 74/2018-Central Tax dated 31.12.2018: Exemption to specified goods from e-Way Bill requirements

- Notification No. 11/2023-Central Tax dated 31.03.2023: Extension of validity for Over Dimensional Cargo

- Notification No. 18/2023-Central Tax dated 01.08.2023: State-specific threshold limit increase

By leveraging these resources, businesses can ensure accurate interpretation and implementation of e-Way Bill provisions, thereby ensuring compliance and avoiding penalties. It’s advisable to consult with a qualified GST professional for specific business scenarios or complex transactions to ensure full compliance with the law.

For Detailed FAQs on E-Way Bill Compliance, Visit the Links Below:

We’ve compiled a comprehensive two-part FAQ series addressing the most frequently asked questions on E-Way Bill under GST, specially curated for businesses, transporters, and GST professionals.

🔹 E-Way Bill – Top FAQs Answered (Part 1): Covers the basics, threshold limits, generation process, and vehicle requirements.

🔹 E-Way Bill – Top FAQs Answered (Part 2): Explains cancellation, extension, multiple consignments, penalties, and advanced queries.

Great insight. Well done.