Table of Contents

Introduction

The digitization of India’s tax system reached a significant milestone with the introduction of electronic invoicing, commonly known as E-Invoice. This revolutionary system has fundamentally transformed how businesses handle their invoicing processes under the Goods and Services Tax (GST) framework. What started as a measure to enhance tax compliance has evolved into a comprehensive digital infrastructure that affects millions of businesses across the country.

E-Invoice represents more than just a technological upgrade—it’s a paradigm shift toward transparency, efficiency, and real-time reporting in India’s taxation ecosystem. The system mandates businesses to generate invoices through a centralized portal, ensuring standardized formats and immediate validation. This isn’t merely about compliance; it’s about creating a seamless, interconnected business environment where data flows effortlessly between taxpayers and tax authorities.

The journey of E-Invoice implementation has been gradual yet decisive. Starting with large enterprises and progressively expanding to smaller businesses, the government has demonstrated a measured approach to digital transformation. Understanding these requirements isn’t optional anymore—it’s essential for survival in today’s business landscape.

Understanding E-Invoice: Legal Framework and Definition

Electronic invoicing under GST is governed by Rule 48 of the Central Goods and Services Tax Rules, 2017, which mandates specific categories of registered persons to prepare invoices in a prescribed manner and report them to the Invoice Registration Portal (IRP). The legal definition encompasses far more than simple digitization of paper invoices.

Section 31 of the CGST Act, 2017, lays the foundation for tax invoice requirements, while subsequent rules and notifications have shaped the E-Invoice ecosystem. The system operates on a standardized schema that ensures uniformity across all business transactions, regardless of industry or size.

The E-Invoice system generates a unique Invoice Reference Number (IRN) for each invoice, which serves as a digital fingerprint. This IRN, along with a digitally signed QR code, becomes the legal proof of the invoice’s authenticity. The process isn’t just about generating numbers—it’s about creating an immutable record that can be verified instantly by any stakeholder in the supply chain.

What makes this system particularly robust is its integration with other GST return forms. Once an invoice receives an IRN, the data automatically populates into the taxpayer’s GSTR-1 return, eliminating manual data entry and reducing the possibility of errors. This seamless integration represents a significant leap forward in tax administration efficiency.

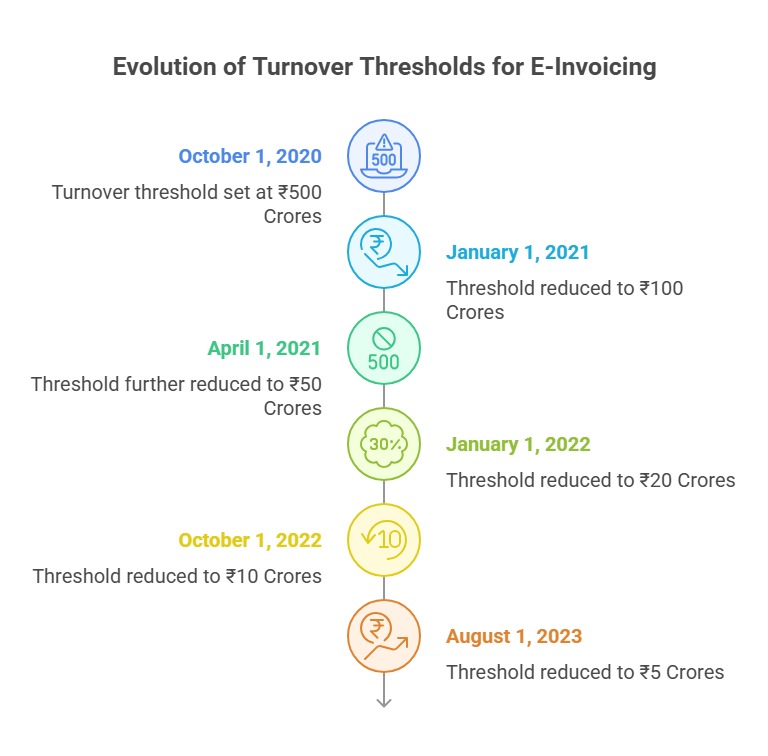

Evolution of E-Invoice Turnover Thresholds

The implementation of E-Invoice has followed a phased approach, with turnover thresholds gradually reducing to include more businesses within its ambit. This strategic rollout allowed the system to mature while providing businesses adequate time to adapt to the new requirements.

Historical Timeline and Threshold Changes

Effective Date | Turnover Threshold | Notification/Circular Reference | Key Provisions |

October 1, 2020 | ₹500 Crores | Notification No. 70/2020-Central Tax dated September 30, 2020 | Initial implementation for large enterprises |

January 1, 2021 | ₹100 Crores | Notification No. 88/2020-Central Tax dated December 30, 2020 | Expansion to mid-size enterprises |

April 1, 2021 | ₹50 Crores | Notification No. 05/2021-Central Tax dated March 29, 2021 | Further expansion covering more businesses |

January 1, 2022 | ₹20 Crores | Notification No. 17/2021-Central Tax dated August 30, 2021 | Significant expansion to smaller enterprises |

October 1, 2022 | ₹10 Crores | Notification No. 14/2022-Central Tax dated July 5, 2022 | Major expansion affecting numerous businesses |

August 1, 2023 | ₹5 Crores | Notification No. 10/2023-Central Tax dated July 10, 2023 | Current threshold covering majority of registered taxpayers |

This systematic reduction demonstrates the government’s commitment to comprehensive digital transformation. Each phase provided valuable insights into system performance and user adoption, allowing for continuous improvements and refinements.

The transition from ₹500 crores to ₹5 crores over less than three years represents one of the most ambitious digitization projects in Indian taxation history. This wasn’t merely about compliance—it was about building a foundation for a completely digital economy where every transaction leaves a verified trail.

Current Legal Requirements and Compliance Framework

Under the current framework, all registered persons with an aggregate turnover exceeding ₹5 crores in any financial year from 2017-18 onwards must comply with E-Invoice requirements. This threshold applies to B2B invoices, exports, and deemed exports, creating a comprehensive coverage of commercial transactions.

The legal obligation extends beyond mere invoice generation. Rule 48(4) of the CGST Rules mandates that the invoice details must be uploaded to the IRP in the prescribed format before the invoice is issued to the recipient. This means businesses cannot issue invoices without first obtaining the IRN and QR code from the system.

Notification No. 10/2023-Central Tax, dated July 10, 2023, brought the threshold down to ₹5 crores, significantly expanding the taxpayer base required to comply with E-Invoice provisions. This notification also clarified various technical aspects and provided necessary exemptions for specific categories of transactions.

The compliance framework requires businesses to integrate their ERP systems with the IRP either directly or through GST Suvidha Providers (GSPs). This integration isn’t optional—it’s a fundamental requirement for maintaining business operations within the legal framework.

Technical Architecture and System Integration

The E-Invoice system operates on a sophisticated technical architecture that ensures reliability, scalability, and security. The Invoice Registration Portal serves as the central hub where all invoice data is validated, processed, and assigned unique identifiers.

When a business generates an invoice, the system performs multiple validation checks including GSTIN verification, HSN code validation, and mathematical accuracy of tax calculations. Only after successful validation does the system generate the IRN and QR code. This process typically takes just a few seconds, but the underlying checks are comprehensive.

The QR code generated contains encrypted invoice details that can be read by any standard QR code reader. This feature enables quick verification of invoice authenticity by recipients, tax authorities, and other stakeholders. The digital signature embedded in the QR code ensures that any tampering with the invoice can be immediately detected.

Integration with existing business systems requires careful planning and execution. Most modern ERP systems now offer built-in E-Invoice functionality, but businesses using older systems may need to invest in upgrades or third-party solutions. The API-based integration allows for real-time invoice processing, ensuring that business operations remain smooth and efficient.

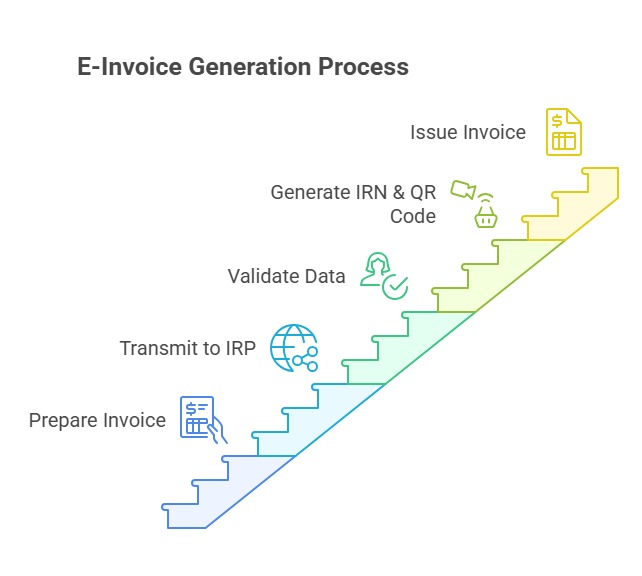

Step-by-Step E-Invoice Generation Process

The E-Invoice generation process follows a standardized workflow that ensures consistency across all implementations. Understanding this process is crucial for businesses to design their systems and train their personnel effectively.

First, the business prepares the invoice in the prescribed JSON format containing all mandatory fields as specified in the E-Invoice schema. This includes basic invoice details, party information, item details with HSN codes, tax calculations, and any applicable additional information.

The prepared invoice data is then transmitted to the IRP through authenticated channels. The system performs real-time validation of all data elements, checking for consistency, accuracy, and compliance with GST rules. Any errors or discrepancies are immediately flagged, requiring correction before processing can continue.

Upon successful validation, the IRP generates a unique IRN and creates a digitally signed QR code containing essential invoice information. The system also generates a JSON response containing the IRN, QR code, and a digitally signed invoice copy that can be used for compliance purposes.

The final step involves incorporating the IRN and QR code into the physical or digital invoice before issuing it to the recipient. This completed invoice serves as the legal document for the transaction and automatically populates the relevant GST return forms.

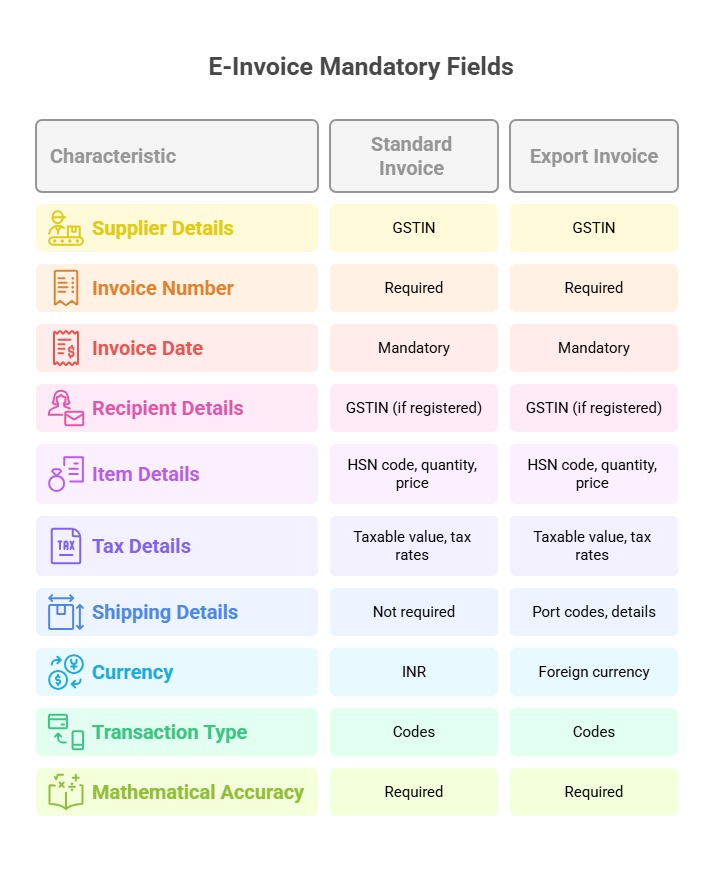

Document Requirements and Mandatory Fields

E-Invoice compliance requires specific mandatory fields that must be included in every invoice. These requirements are detailed in the E-Invoice schema and are strictly enforced by the validation system.

Essential fields include the supplier’s GSTIN, invoice number, invoice date, recipient details with GSTIN (for registered recipients), item-wise details with HSN codes, quantity, unit price, taxable value, and applicable tax rates. Each field has specific formatting requirements and validation rules that must be followed precisely.

For export invoices, additional fields become mandatory, including port codes, shipping details, and foreign currency information. The system also requires specific codes for different types of transactions, such as regular sales, deemed exports, or SEZ supplies.

The invoice must also include mathematical accuracy in tax calculations. The system validates that the sum of taxable values, tax amounts, and final invoice value are all correctly calculated. Any discrepancy, even of a single paisa, will result in rejection of the invoice.

Benefits and Advantages of E-Invoice Implementation

The E-Invoice system has delivered significant benefits to businesses, tax authorities, and the broader economy. These advantages extend far beyond simple compliance, creating value throughout the business ecosystem.

For businesses, the most immediate benefit is the elimination of manual data entry in GST returns. Once an invoice receives an IRN, the data automatically flows into GSTR-1, reducing preparation time and minimizing errors. This automation has saved countless hours of accounting work and reduced the likelihood of mismatches between invoices and returns.

The system has also enhanced the credibility of invoices in the market. The IRN and QR code provide instant verification of invoice authenticity, reducing disputes and improving trust between trading partners. Banks and financial institutions increasingly rely on E-Invoice data for credit decisions, making it easier for businesses to access financing.

From a tax administration perspective, E-Invoice has provided unprecedented visibility into commercial transactions. The real-time data capture enables better analytics, improved compliance monitoring, and more targeted enforcement actions. This visibility helps in identifying tax evasion patterns and ensuring that legitimate businesses aren’t disadvantaged by unfair competition.

The reduction in fake invoices has been another significant benefit. The validation requirements and real-time processing make it extremely difficult to generate fraudulent invoices, protecting the tax base and ensuring fair competition in the market.

Common Challenges and Implementation Issues

Despite its benefits, E-Invoice implementation has not been without challenges. Many businesses have faced technical difficulties, process disruptions, and compliance concerns during the transition period.

Integration with existing ERP systems has been one of the most significant challenges. Older systems often lack the flexibility to accommodate E-Invoice requirements, forcing businesses to invest in expensive upgrades or workarounds. The JSON format requirement has also posed difficulties for businesses using simple accounting software.

Network connectivity and system downtime have caused operational disruptions. Since E-Invoice generation requires real-time connectivity to the IRP, any network issues can halt invoice processing. The system has experienced periodic downtime during peak usage periods, affecting business operations.

Training and awareness have been ongoing challenges. The technical nature of E-Invoice requirements means that accounting personnel need specialized training to handle the system effectively. Many businesses have struggled with the learning curve, leading to errors and compliance issues.

The cost of compliance has also been a concern, particularly for smaller businesses near the threshold. The investment in system upgrades, training, and ongoing maintenance can be substantial, affecting profitability and cash flow.

Exemptions and Special Cases

The E-Invoice framework includes several exemptions and special provisions that businesses must understand to ensure proper compliance. These exemptions are specifically detailed in various notifications and circulars issued by the tax authorities.

Certain categories of registered persons are exempt from E-Invoice requirements regardless of their turnover. These include special economic zone units, persons paying tax under composition scheme, and those dealing exclusively in exempted goods or services.

Specific types of invoices are also exempt from E-Invoice requirements. These include invoices issued to unregistered persons (B2C transactions), credit notes, debit notes, and invoices for services provided by way of transportation of goods by road.

Banking and financial services have special considerations. While banks are generally covered under E-Invoice requirements, certain specific transactions like ATM cash withdrawals and some regulatory compliance transactions may have different treatment.

Government entities and public sector undertakings may have modified requirements or exemptions depending on their specific operational needs and statutory obligations.

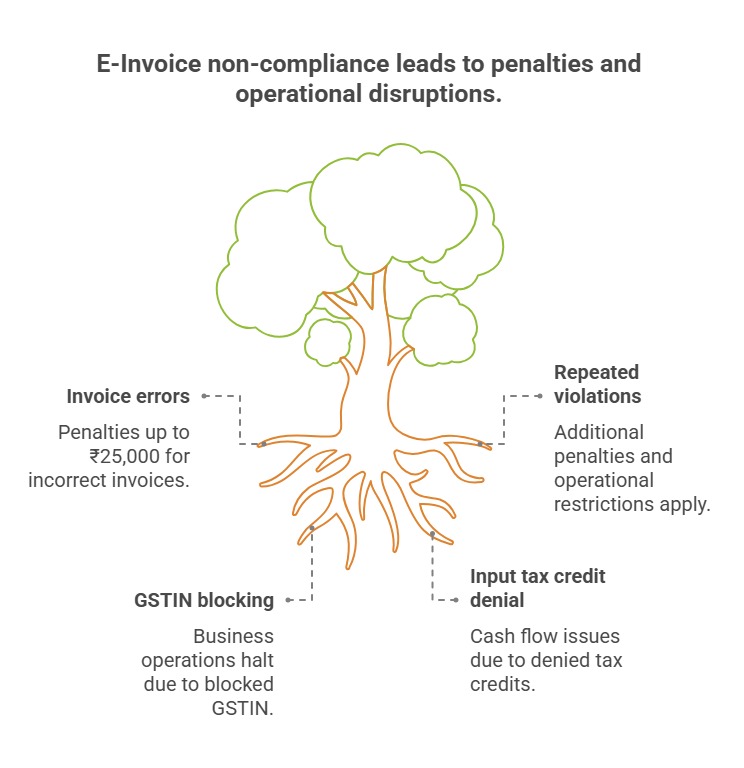

Penalties and Consequences of Non-Compliance

Non-compliance with E-Invoice requirements can result in significant penalties and operational difficulties. The penalty structure is designed to ensure compliance while providing reasonable opportunity for rectification.

Section 125 of the CGST Act provides the framework for penalties related to invoice-related violations. Failure to issue invoices in the prescribed manner can result in penalties up to ₹25,000. For repeated violations, additional penalties and restrictions may apply.

Beyond monetary penalties, non-compliance can result in blocking of GSTIN, which effectively prevents the business from conducting normal commercial operations. This administrative action can have severe consequences for business continuity and reputation.

The input tax credit implications are also significant. Invoices without proper IRN may not be accepted for input tax credit purposes, affecting the cash flow and tax liability of recipient businesses. This creates a cascading effect throughout the supply chain.

Best Practices for E-Invoice Compliance

Successful E-Invoice implementation requires careful planning, proper system design, and ongoing maintenance of compliance processes. Businesses that have successfully navigated the transition share several common best practices.

System integration should be planned well in advance of the compliance deadline. This includes evaluating current ERP capabilities, identifying gaps, and implementing necessary upgrades. Testing should be conducted thoroughly in a sandbox environment before going live.

Training programs for accounting and IT personnel are essential. The technical nature of E-Invoice requirements means that staff need specialized knowledge to handle the system effectively. Regular training updates are necessary as the system evolves and new features are introduced.

Backup systems and contingency plans are crucial for business continuity. Since E-Invoice generation is mandatory, businesses need reliable backup internet connections and alternative processing methods to handle system outages or technical difficulties.

Regular monitoring and reconciliation of E-Invoice data with accounting records helps identify and resolve discrepancies quickly. This proactive approach prevents accumulation of errors and ensures smooth compliance.

Future Developments and System Enhancements

The E-Invoice system continues to evolve with regular updates and enhancements based on user feedback and technological advancement. Understanding the roadmap helps businesses prepare for future changes and opportunities.

Integration with other government systems is expanding. The E-Invoice data is increasingly being used for various compliance requirements including income tax, customs, and regulatory filings. This integration reduces the compliance burden while improving data accuracy across government systems.

Enhanced analytics and reporting capabilities are being developed to provide businesses with better insights into their transaction patterns and compliance status. These tools will help businesses optimize their operations and identify potential issues before they become problems.

Mobile applications and simplified interfaces are being developed to make the system more accessible to smaller businesses and those with limited technical resources. These developments will democratize access to E-Invoice benefits across the business spectrum.

Artificial intelligence and machine learning capabilities are being integrated to improve validation accuracy and provide predictive insights. These enhancements will make the system more intelligent and user-friendly while maintaining security and compliance standards.

International Perspective and Comparative Analysis

India’s E-Invoice system is part of a global trend toward digital taxation and real-time reporting. Comparing the Indian approach with international implementations provides valuable context and insights.

The European Union has been working on standardized electronic invoicing requirements across member states. While the approach differs from India’s centralized model, the objectives of reducing compliance costs and improving tax administration are similar.

Latin American countries like Brazil and Mexico have implemented electronic invoicing systems with varying levels of success. These experiences provide valuable lessons about system design, implementation strategies, and user adoption challenges.

The real-time reporting aspect of India’s E-Invoice system is more comprehensive than many international implementations. This approach provides immediate visibility to tax authorities but requires more sophisticated technical infrastructure and higher compliance standards.

Sector-Specific Considerations

Different industry sectors face unique challenges and opportunities in E-Invoice implementation. Understanding these sector-specific considerations helps businesses develop targeted compliance strategies.

Manufacturing companies with complex supply chains benefit significantly from E-Invoice automation. The integration with inventory management and production planning systems can provide real-time visibility into costs and margins.

Service sector businesses face different challenges, particularly in defining taxable events and invoice timing. Professional services, consulting, and IT companies need to carefully map their billing processes to E-Invoice requirements.

Trading businesses with high transaction volumes need robust systems capable of handling large-scale E-Invoice generation. The automation benefits are significant, but the initial investment in system capability can be substantial.

Export-oriented businesses have additional compliance requirements and benefit from the integrated reporting capabilities that eliminate duplicate data entry across various export documentation requirements.

Technology Considerations and System Requirements

Successful E-Invoice implementation requires careful consideration of technical requirements and system capabilities. Understanding these requirements helps businesses make informed decisions about technology investments.

API integration capabilities are fundamental for seamless E-Invoice processing. Businesses need systems that can handle real-time communication with the IRP while maintaining data security and integrity.

Data backup and recovery systems become critical when E-Invoice processing is integrated into core business operations. Any system failure that prevents invoice generation can halt business operations entirely.

Security considerations include protecting sensitive business data while ensuring compliance with E-Invoice transmission requirements. This balance requires sophisticated security protocols and regular security updates.

Scalability planning is essential for growing businesses. Systems should be designed to handle increasing transaction volumes without performance degradation or compliance failures.

Conclusion

The E-Invoice system under GST represents a fundamental transformation in how businesses handle invoicing and compliance in India. From its initial implementation for businesses with turnover above ₹500 crores to the current threshold of ₹5 crores, the system has demonstrated the government’s commitment to digital transformation and improved tax administration.

The journey has not been without challenges. Businesses have had to invest in new systems, train personnel, and adapt processes to meet the technical requirements. However, the benefits have become increasingly apparent as the system has matured and businesses have gained experience with its operation.

The reduction in manual processing, improved accuracy in GST returns, enhanced invoice credibility, and better access to credit facilities have created tangible value for businesses. The elimination of fake invoices and improved compliance monitoring have strengthened the overall tax system.

Looking forward, the E-Invoice system will continue to evolve with enhanced features, better integration, and improved user experience. The expansion to smaller businesses through threshold reductions will democratize these benefits across the entire business ecosystem.

For businesses still adapting to E-Invoice requirements, the key is to approach implementation strategically. This means investing in proper systems, training personnel thoroughly, and maintaining focus on compliance while leveraging the operational benefits the system provides.

The E-Invoice system is more than a compliance requirement—it’s an opportunity to modernize business processes, improve operational efficiency, and participate fully in India’s digital economy. Businesses that embrace this transformation will find themselves better positioned for future growth and success in an increasingly digital marketplace.

Understanding and implementing E-Invoice requirements is no longer optional for businesses exceeding the threshold limits. It’s a fundamental requirement for legal operation and a pathway to improved business efficiency. The investment in proper implementation will continue to deliver returns through improved processes, reduced errors, and enhanced business credibility in the evolving digital economy.

Stay updated with the latest GST changes—Follow TaxGroww for expert insights and compliance updates!