Table of Contents

Introduction

The vast majority of business owners find out the hard way how this works: you are charged a fee for hiring an attorney to give you legal advice; and you end up being responsible for paying the GST yourself – NOT the attorney. Or you rent office space from a landlord who has never heard of GST Registration (and therefore has no idea about GST) – but somehow you are still on the hook for all the tax owed on the lease payments you made to him. You see – confusing, right? That is RCM as it relates to GST for you.

The Reverse Charge Mechanism, or RCM under GST, does exactly what it says—reverses who pays the tax. Normally, sellers collect GST from buyers and hand it over to the government. Makes sense, right? But under RCM under GST, that logic gets flipped. The buyer pays the tax directly to the government instead. Why? Because the government figured out that in certain situations—dealing with unregistered suppliers, small vendors, or specific service categories—getting the seller to comply is practically impossible.

Now, here’s where it gets tricky. RCM under GST doesn’t apply to everything. It’s selective. There are notified lists—goods and services specifically mentioned by the government. Miss one of these, and you’re looking at penalties, interest charges, and possibly losing your Input Tax Credit. The frustrating part? Even seasoned businesses sometimes miss RCM under GST obligations because the provisions are scattered across multiple sections, notifications keep changing, and frankly, the documentation requirements feel excessive.

This isn’t another superficial overview. If you’re dealing with purchases from unregistered dealers, hiring professionals like advocates or directors, renting property, or receiving government services, RCM under GST probably affects you. This guide breaks down everything—from identifying when RCM under GST applies to handling the cash flow complications it creates. Because understanding this mechanism isn’t optional anymore. It’s essential.

Understanding RCM Under GST: The Basics

RCM under GST represents a fundamental departure from normal tax mechanics. To grasp its significance, we must first understand what makes it different.

The Definition

Section 2(98) of the Central Goods and Services Tax Act, 2017 defines “reverse charge” as the liability to pay tax by the recipient of supply instead of the supplier. This statutory definition forms the backbone of RCM under GST provisions.

Under normal circumstances, suppliers collect GST from customers and deposit it with authorities. The tax invoice issued by suppliers includes GST amount, which customers pay along with the base price. Suppliers then file returns and remit collected taxes.

RCM under GST reverses this completely. The recipient becomes responsible for calculating tax, depositing it directly with the government, and reporting it in their returns. The supplier issues invoices without collecting GST, sometimes not even issuing formal tax invoices.

Why RCM Under GST Law

The legislative intent behind RCM under GST serves multiple objectives. First, it tackles sectors where suppliers are numerous, small-scale, or operate below registration thresholds. Consider agriculture—expecting thousands of farmers to register, invoice, and file returns creates administrative impossibility.

Second, RCM under GST prevents revenue leakage. When dealing with suppliers likely to evade compliance, shifting responsibility to established, registered recipients ensures tax collection. The government relies on larger businesses having better compliance infrastructure.

Third, certain transactions—like government services or imports—benefit from simplified collection through RCM under GST. Rather than making government departments manage outward GST compliance, placing liability on business recipients streamlines the process.

Three Scenarios of RCM Under GST

RCM under GST operates through three distinct legal provisions, each addressing different situations:

First Scenario – Notified Supplies: Covered by Section 9(3) of CGST/SGST Act and Section 5(3) of IGST Act, this involves specific goods and services notified by the government. The notification specifies exact categories where RCM under GST applies regardless of supplier registration status.

Second Scenario – Unregistered to Registered: Section 9(4) of CGST/SGST Act and Section 5(4) of IGST Act originally covered all supplies from unregistered persons to registered persons. However, subsequent notifications have limited its practical application to specific supplies only.

Third Scenario – E-commerce Transactions: Section 9(5) of CGST/SGST Act and Section 5(5) of IGST Act make electronic commerce operators liable for certain specified services. The platform collecting payments becomes responsible for GST, implementing a form of RCM under GST.

Legal Provisions Governing RCM Under GST

Understanding the legal framework helps identify obligations and navigate compliance requirements effectively.

Section 9(3) and Section 5(3) - The Notification Mechanism

These provisions empower the government to notify specific supplies attracting RCM under GST. The language is permissive: “The Government may, on recommendations of the Council, by notification, specify categories…”

This means RCM under GST doesn’t apply automatically to any supply. Only specifically notified categories trigger reverse charge obligations. Currently, notifications specify ten goods categories and sixteen services categories where RCM under GST applies.

The notification mechanism provides flexibility. As market conditions change or compliance patterns evolve, the government can add or remove items from RCM under GST lists. Recent amendments demonstrate this—sponsorship services were removed from RCM under GST effective January 2025.

Section 9(4) and Section 5(4) - Unregistered Supplier Provisions

These sections originally created widespread concern. The literal reading suggested all purchases from unregistered persons would attract RCM under GST. A small business buying office supplies from an unregistered vendor would face reverse charge compliance.

Recognizing the impracticality, the government issued exemptions. Currently, RCM under GST applies to unregistered-to-registered supplies only for notified categories. For most regular business purchases from unregistered vendors, forward charge applies—the supplier pays tax if their turnover exceeds registration thresholds.

Section 9(5) and Section 5(5) - E-commerce Operator Liability

Modern commerce increasingly flows through digital platforms. Thousands of individual service providers—cab drivers, restaurant owners, accommodation providers—operate through aggregator apps. Expecting each individual to handle GST compliance creates chaos.

RCM under GST provisions for e-commerce solve this elegantly. The platform operator becomes liable for collecting and paying tax. Individual service providers need not register or file returns. The operator aggregates all transactions and handles compliance centrally.

This applies specifically to notified services: passenger transportation (excluding certain omnibus services), accommodation services, housekeeping services, and restaurant services (with specific exclusions). The e-commerce operator effectively becomes the supplier for GST purposes.

Notified Goods Attracting RCM Under GST

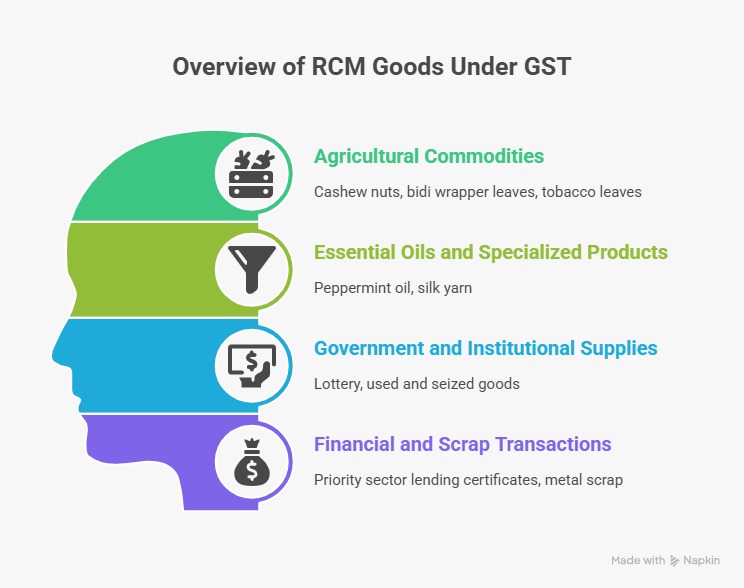

Ten distinct goods categories fall under RCM under GST, each reflecting specific policy considerations.

Agricultural Commodities

Three agricultural products feature in RCM under GST lists:

Cashew Nuts (Not Shelled or Peeled): When agriculturists supply raw cashew nuts to any registered person, RCM under GST applies. The processing industry typically purchases from numerous small farmers. Rather than requiring each farmer to register and comply, the burden shifts to the processor.

Bidi Wrapper Leaves (Tendu): These leaves, essential for bidi manufacturing, come primarily from forest-dwelling communities and small collectors. RCM under GST ensures tax collection at the manufacturer level rather than from scattered suppliers.

Tobacco Leaves: Similar to cashew and tendu, tobacco cultivation involves numerous small agriculturists. RCM under GST places compliance responsibility on registered buyers—typically manufacturers or traders with established systems.

The common thread? All three involve unorganized supply chains where tracking individual supplier compliance becomes impractical. RCM under GST concentrates liability at the organized buyer level.

Essential Oils and Specialized Products

Essential Oils: Peppermint oil, spearmint oil, water mint oil, horsemint oil, bergamot oil, and mentha arvensis oils attract RCM under GST when supplied by unregistered persons. These products serve pharmaceutical, cosmetic, and food industries where buyers typically maintain registration.

Silk Yarn: Manufacturers producing silk yarn from raw silk or silkworm cocoons fall under RCM under GST when supplying to registered persons. This provision targets the silk industry’s specific structure where yarn production often occurs in small-scale units supplying larger manufacturers or traders.

Government and Institutional Supplies

Lottery: State Governments, Union Territories, or local authorities supplying lottery to distributors or selling agents must follow RCM under GST. This ensures tax collection at the wholesale distribution level rather than scattered retail points.

Used and Seized Goods: Central Government (excluding Ministry of Railways), State Governments, Union Territories, or local authorities selling used vehicles, seized goods, confiscated items, old goods, waste, or scrap trigger RCM under GST. The registered purchaser pays tax.

These provisions address government auction sales where applying standard GST collection mechanisms proves difficult.

Financial and Scrap Transactions

Priority Sector Lending Certificates: These tradeable instruments used by banks to meet regulatory requirements attract RCM under GST when transacted between registered persons. The buyer pays tax on reverse charge.

Metal Scrap: Any unregistered person supplying metal scrap falling under specified chapters (72-81 covering various metals) to registered persons triggers RCM under GST. This provision significantly impacts manufacturing units, recycling facilities, and scrap traders dealing with unorganized suppliers.

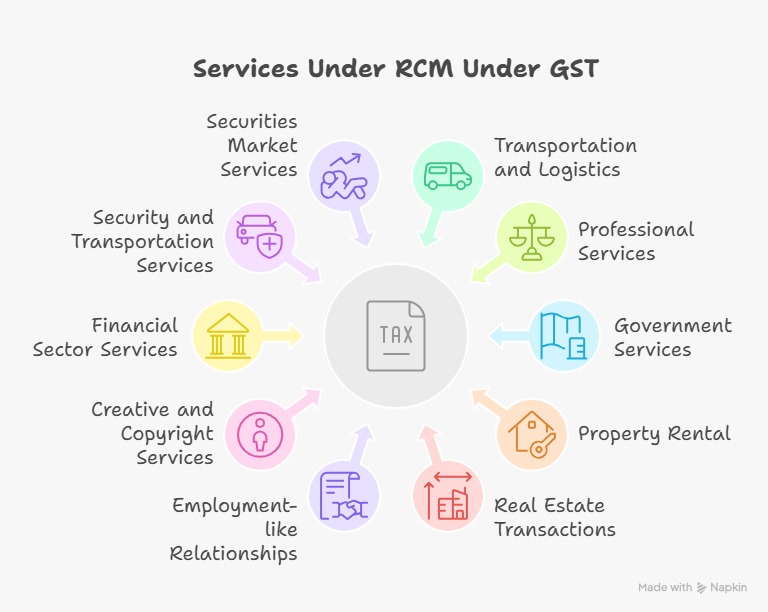

Services Covered Under RCM Under GST

Sixteen service categories attract RCM under GST, each addressing distinct compliance scenarios.

Transportation and Logistics

Goods Transport Agency Services: When specified entities hire GTAs for road freight, RCM under GST typically applies. Specified entities include factories, registered persons, corporate bodies, partnership firms, and casual taxable persons.

However, GTAs can opt out of RCM under GST by fulfilling certain conditions and charging tax under forward charge. Many established GTAs exercise this option to maintain competitive positioning.

Professional Services

Legal Services: Individual advocates, senior advocates, or advocate firms providing legal services to business entities trigger RCM under GST. This covers advice, consultancy, assistance in any legal branch, and representational services before courts or tribunals.

The rationale recognizes that many legal practitioners operate as individuals without separate business structures. Placing RCM under GST on business clients simplifies compliance.

Arbitration Services: Arbitral tribunals providing services to business entities fall under RCM under GST. Arbitration increasingly resolves commercial disputes, and this provision ensures tax collection regardless of tribunal registration status.

Government Services

Services by Government Entities: Central Government, State Governments, Union Territories, or local authorities providing services to business entities generally attract RCM under GST. Significant exclusions exist:

- Renting of immovable property (covered separately)

- Services by Department of Posts

- Services by Ministry of Railways

- Aircraft or vessel related services

- Transportation of goods or passengers

This provision ensures government departments don’t navigate complex outward supply compliance. Business recipients handle tax payment.

Property Rental Under RCM Under GST

Multiple provisions govern rentals:

Government Property Rental: When government entities rent immovable property to registered persons, RCM under GST applies. This covers office spaces, commercial properties, or any immovable property leased by government departments.

Residential Dwelling Rental: Any person renting residential property to a registered person faces RCM under GST. This significantly impacts businesses renting accommodations for employees, guest houses, or director residences.

Non-residential Property by Unregistered Persons: Unregistered landlords renting non-residential property to registered persons (excluding composition taxpayers) trigger RCM under GST. Office rentals, warehouse leases, or commercial space rentals from unregistered landlords fall here.

These provisions have created considerable compliance burden, particularly for small businesses renting from individual property owners who lack GST awareness.

Real Estate Transactions

Development Rights and FSI: Promoters receiving development rights or Floor Space Index (including additional FSI) for construction projects face RCM under GST. The supplier—often land owners or development authorities—doesn’t collect tax.

Long-term Land Lease: Leases of 30 years or more with upfront premiums and periodic rent for construction projects attract RCM under GST. This targets real estate development where land acquisition involves long-term lease arrangements.

Both provisions ensure tax collection on high-value real estate transactions where suppliers might otherwise avoid registration.

Employment-like Relationships

Director Services: Directors providing services to their companies trigger RCM under GST. The company pays tax on reverse charge for director remuneration classified as services.

Insurance Agents: Insurance agents serving insurance companies fall under RCM under GST. The insurance company handles tax payment rather than individual agents.

Recovery Agents: Recovery agents working for banks, financial institutions, or NBFCs trigger RCM under GST. The financial institution pays tax.

These provisions recognize relationships where recipients have better administrative capacity for compliance than individual service providers.

Creative and Copyright Services

Music, Photography, and Artistic Services: Musicians, photographers, or artists transferring copyrights of original dramatic, musical, or artistic works to music companies or producers face RCM under GST.

Literary Works by Authors: Authors transferring literary work copyrights to publishers trigger RCM under GST. However, authors can opt for forward charge by registering, filing declarations, and complying with specified conditions.

These provisions address creative industries where individual creators often operate without formal business structures.

Financial Sector Services

Direct Selling Agents: Individual DSAs (not corporate entities or firms) serving banks or NBFCs fall under RCM under GST. The bank or NBFC pays tax.

Business Facilitators: Business facilitators working with banks trigger RCM under GST, with banks handling compliance.

Business Correspondent Agents: Agents of business correspondents providing services to BCs face RCM under GST.

These provisions address the extensive agent networks in banking and financial services.

Security and Transportation Services

Security Services: Non-corporate entities providing security personnel supply services to registered persons under RCM under GST. Specific exclusions exist for government departments and composition taxpayers receiving such services.

Motor Vehicle Rental with Fuel: Non-corporate entities renting passenger motor vehicles to corporate bodies with fuel costs included trigger RCM under GST if they don’t charge tax at specified rates under forward charge.

Securities Market Services

Securities Lending: Under SEBI’s Securities Lending Scheme, 1997, lenders depositing securities with approved intermediaries for borrowing trigger RCM under GST. The borrower pays tax on reverse charge.

Recent Amendment - Sponsorship Services Removed

Until January 16, 2025, sponsorship services provided by individuals or non-corporate entities to corporate bodies or partnership firms attracted RCM under GST. Notification No. 07/2025-Central Tax (Rate) removed this provision.

Now sponsorship service providers must charge and collect GST under forward charge. This change reduces RCM under GST scenarios for many businesses while ensuring suppliers handle compliance.

Time of Supply for RCM Under GST

Determining when tax liability arises—the time of supply—follows specific rules under RCM under GST provisions.

For Goods Under RCM Under GST

Section 12(3) of the CGST Act specifies that time of supply for goods under reverse charge is the earliest of:

Receipt Date: When the recipient physically receives goods, liability crystallizes immediately.

Payment Date: The date appearing in the recipient’s books of account or bank account debit date, whichever occurs first.

31st Day After Invoice: If neither receipt nor payment happens, the day immediately following 30 days from invoice date (or similar document date) becomes the time of supply.

Book Entry Date: When none of the above can be determined, the date of entry in recipient’s books governs.

For Services Under RCM Under GST

Section 12(4) of the CGST Act specifies time of supply for services under reverse charge as the earliest of:

Payment Date: As recorded in books or bank debit date, whichever is earlier.

61st Day After Invoice: If payment doesn’t occur, the day immediately following 60 days from invoice date determines liability.

Book Entry Date: When neither can be ascertained, book entry date applies.

Practical Examples

Example 1 – Legal Services: A company engages an advocate on March 1st. The advocate’s invoice is dated February 28th. The company pays on March 20th. The time of supply under RCM under GST is March 20th (payment date).

Example 2 – Delayed Payment: Using the same facts, if payment delays beyond April 28th (60 days from invoice), April 29th automatically becomes the time of supply for RCM under GST regardless of when payment actually occurs.

Example 3 – Advance Payment: If the company pays ₹50,000 advance on February 15th before even engaging services, February 15th becomes the time of supply for RCM under GST on the advance amount.

Compliance Implications

These provisions mean businesses must monitor multiple dates simultaneously. Internal controls should flag RCM under GST transactions immediately upon occurrence. Setting reminders for the 30-day (goods) or 60-day (services) limits prevents inadvertent late compliance.

Late payment beyond time of supply triggers interest liability at 18% per annum, even if tax gets paid eventually.

Registration Requirements for RCM Under GST

One of RCM under GST’s most significant compliance impacts involves mandatory registration.

Threshold Exemption Doesn't Apply

Section 24 of the CGST Act lists persons requiring compulsory registration. Section 24(ix) specifically includes “persons who are required to pay tax under reverse charge.”

This means even if a business’s total turnover stays below ₹40 lakhs (or ₹20 lakhs for special category states), any liability under RCM under GST triggers mandatory registration.

Practical Impact

Consider a startup with annual turnover of ₹30 lakhs. Normally, no GST registration would be required. However, if this startup:

- Hires an advocate for ₹50,000

- Rents office space from an unregistered landlord for ₹25,000 monthly

- Purchases services worth ₹75,000 from an unregistered consultant

Any single transaction attracting RCM under GST creates mandatory registration obligation. The startup must register, comply with all GST provisions, and handle RCM under GST for these transactions.

Burden on Small Businesses

This creates significant compliance burden for small entities. Many businesses face registration requirements solely due to occasional RCM under GST transactions, not their own supply activities.

The requirement applies even to composition scheme taxpayers. While composition scheme offers simplified compliance for small businesses, it doesn’t exempt RCM under GST obligations. In fact, composition taxpayers cannot receive certain RCM under GST supplies like security services.

No Exemptions

Unlike normal GST where various exemptions and special provisions exist, RCM under GST registration requirements apply universally. No monetary threshold, no sector-specific exemptions, no special considerations—any RCM under GST liability means mandatory registration.

Input Tax Credit Under RCM Under GST

The interaction between RCM under GST and Input Tax Credit involves critical nuances affecting cash flow and tax liability.

Supplier Cannot Claim ITC

Section 17(3) of the CGST Act explicitly restricts suppliers from claiming ITC on inputs used for making supplies where recipients pay tax under RCM under GST.

This makes logical sense. If the supplier isn’t paying output GST (because the recipient handles it under RCM under GST), allowing input credit would mean the supplier gets ITC without corresponding output liability.

Recipient Can Claim ITC - With Conditions

Recipients paying tax under RCM under GST can claim ITC, subject to Section 16 conditions. The key conditions include:

- Possession of valid tax invoice or debit note

- Actual receipt of goods or services

- Tax has been paid to the government

- Returns have been filed

However, one critical requirement distinguishes RCM under GST from regular ITC claims: the recipient must first pay RCM under GST liability through cash (electronic cash ledger). ITC cannot directly discharge RCM under GST liability.

The "Pay First, Claim Later" Mechanism

This creates a specific compliance sequence for RCM under GST:

Step 1: Deposit cash in the electronic cash ledger

Step 2: Pay RCM under GST liability using this cash balance

Step 3: Report payment in GSTR-3B Table 3.1(d)

Step 4: Claim the same amount as ITC in GSTR-3B Table 4(A)(3)

The net impact becomes neutral eventually—tax paid equals credit claimed. However, cash outflow occurs first, creating working capital implications.

Practical Example

A company receives legal services worth ₹1,00,000. GST at 18% means ₹18,000 RCM under GST liability.

Traditional Thinking (Incorrect): Use ₹18,000 from existing ITC balance to pay RCM under GST.

Actual Requirement:

- Deposit ₹18,000 cash in electronic cash ledger

- Pay RCM under GST using this cash

- Later claim ₹18,000 as ITC

For businesses with tight cash flows, this creates temporary cash deployment requirements despite ultimate neutrality.

ITC Eligibility Conditions

Even after paying RCM under GST in cash, ITC claim requires satisfying normal eligibility conditions:

- The goods or services must be used for business purposes

- The goods or services must be used for making taxable supplies (not exempt supplies)

- The supplier must file GSTR-1 reporting the outward supply (where applicable)

Blocked credits under Section 17(5) apply equally to RCM under GST. If the supply falls under blocked credit categories (like food and beverages, outdoor catering, health services for employees), no ITC is available despite paying RCM under GST.

Compliance and Documentation for RCM Under GST

Handling RCM under GST requires specific documentation and reporting beyond standard GST compliance.

Invoicing Requirements

When suppliers cannot issue tax invoices—typically when they’re unregistered—recipients must create self-invoices for RCM under GST transactions.

Rule 46 of the CGST Rules requires self-invoices to contain all mandatory particulars:

- Supplier’s name, address, and GSTIN (if available)

- Recipient’s name, address, and GSTIN

- Description of goods or services

- Quantity and unit of measurement

- Total value of supply

- Taxable value

- Tax rate and tax amount (CGST, SGST/UTGST, IGST, cess)

- Place of supply

- Whether tax is payable under reverse charge

- Signature or digital signature

The self-invoice serves dual purposes: documentary evidence for RCM under GST payment and basis for claiming ITC.

Invoice Notation Requirements

Even when suppliers issue invoices, Section 31 read with Rule 46 requires clear indication of reverse charge applicability. Invoices should state “Tax payable on reverse charge by recipient” or similar language.

This notation alerts recipients to their RCM under GST obligations and prevents inadvertent non-compliance.

Payment Vouchers

When making payment to suppliers for RCM under GST supplies, recipients should issue payment vouchers. These documents create audit trail linking payment with underlying supply.

Payment vouchers should reference:

- The supply transaction

- Invoice or self-invoice number

- Payment amount

- Payment date

- Bank details

GSTR-1 Reporting by Suppliers

Registered suppliers making RCM under GST supplies report these in GSTR-1 Table 4B. This table requires invoice-level details of all reverse charge supplies including:

- Invoice number and date

- Recipient’s GSTIN and name

- Supply value

- Applicable tax rate

- Whether IGST or CGST/SGST applies

This reporting creates cross-verification mechanism. Tax authorities can match supplier’s GSTR-1 Table 4B entries with recipient’s GSTR-3B RCM under GST reporting.

GSTR-3B Reporting by Recipients

Recipients report RCM under GST in two places within monthly GSTR-3B:

Table 3.1(d) – Tax Payable: Total RCM under GST liability for the month appears here, broken down into:

- Integrated Tax (IGST)

- Central Tax (CGST)

- State/UT Tax (SGST/UTGST)

- Cess

This table reports the liability side of RCM under GST.

Table 4(A)(3) – ITC Available: After paying RCM under GST liability in cash, the same amount gets claimed as ITC here. This table shows:

- Integrated Tax

- Central Tax

- State/UT Tax

- Cess

The amounts in Table 3.1(d) and Table 4(A)(3) should match for RCM under GST transactions where ITC is eligible.

Record Maintenance

Section 35 of the CGST Act requires maintaining true and correct accounts. For RCM under GST, this includes:

- Self-invoices or supplier invoices

- Payment vouchers

- Bank statements showing cash ledger deposits and debits

- Calculation worksheets for tax amounts

- Correspondence regarding supplies

- Copies of GSTR-1 and GSTR-3B

- Any notices or communications from tax authorities

Rule 56 mandates retaining records for six years from the last date of filing annual returns. Given potential scrutiny of RCM under GST compliance, comprehensive record-keeping becomes essential.

Recent Amendments in RCM Under GST

GST provisions evolve through notifications and circulars. Understanding recent changes ensures current compliance with RCM under GST requirements.

January 2025 - Sponsorship Services Removed

Notification No. 07/2025-Central Tax (Rate) dated January 16, 2025, removed sponsorship services from RCM under GST. Previously, individuals or non-corporate persons providing sponsorship to corporate bodies or partnership firms triggered reverse charge.

Post-amendment, sponsorship service providers must charge GST under forward charge. This change:

- Reduces RCM under GST scenarios for recipient businesses

- Places compliance responsibility on service providers

- Simplifies compliance for companies receiving sponsorships

Businesses providing or receiving sponsorship services should update their systems to reflect forward charge treatment effective January 16, 2025.

February 2025 - ISD Compliance Clarification

Notification No. 09/2025-Central Tax dated February 11, 2025, clarified Input Service Distributor compliance regarding RCM under GST.

The notification specifies that ISDs cannot procure supplies attracting RCM under GST in their ISD capacity. If an entity wants to make such purchases and take RCM under GST payment as ITC, it must register as a regular taxpayer, not just as an ISD.

This clarification prevents businesses from routing RCM under GST supplies through ISD registrations to avoid compliance complications.

Earlier Amendments

Exemption Withdrawal: Originally, Notification No. 8/2017-Central Tax (Rate) exempted supplies up to ₹5,000 per day from unregistered dealers from RCM under GST under Section 9(4). Notification No. 1/2019-Central Tax (Rate) subsequently withdrew this exemption.

While the exemption no longer exists, practical enforcement of Section 9(4) RCM under GST currently limits to notified categories rather than all unregistered-to-registered supplies.

GTA Option: Various amendments have refined conditions under which GTAs can opt for forward charge instead of RCM under GST. Currently, GTAs meeting specific criteria can charge tax and pay under forward charge, providing flexibility to both GTAs and recipients.

Common Challenges in RCM Under GST Implementation

Businesses face recurring challenges implementing RCM under GST compliance. Understanding these helps develop effective solutions.

Identification Difficulty

The multiplicity of provisions—Section 9(3), 9(4), 9(5)—combined with extensive notification lists creates identification challenges. Businesses struggle determining which supplies attract RCM under GST.

Solution: Maintain an updated checklist covering all notified goods and services attracting RCM under GST. Review vendor agreements and invoices against this checklist. When onboarding new vendors, verify registration status and supply nature. Implement automated systems that flag potential RCM under GST transactions.

Cash Flow Impact

The requirement to pay RCM under GST in cash before claiming ITC creates working capital constraints. While ultimately neutral, the temporary cash deployment impacts businesses with tight liquidity.

Solution: Plan cash flows considering RCM under GST liabilities. Include estimated RCM under GST amounts in monthly tax provisioning. Maintain adequate cash ledger balance. For predictable RCM under GST obligations (like monthly rent), schedule deposits systematically.

Landlord Cooperation

Property rentals attracting RCM under GST require tenant registration and compliance. Many landlords lack awareness, causing friction when tenants explain they won’t pay GST directly but will deposit it themselves.

Solution: Educate landlords about RCM under GST provisions early in negotiations. Explain that landlords don’t face additional obligations—tenants handle tax payment. Include clear RCM under GST clauses in rental agreements specifying tenant responsibilities. Provide landlords with summary sheets explaining the mechanism.

Documentation Burden

Self-invoicing, payment vouchers, and cross-verification with supplier reporting create significant documentation work for RCM under GST.

Solution: Implement automated systems for RCM under GST identification and documentation. Many GST software packages now include modules that auto-generate self-invoices, calculate tax amounts, and maintain required records. Use templates for payment vouchers to standardize documentation.

Time of Supply Monitoring

Tracking multiple dates—receipt date, payment date, invoice date plus prescribed days—complicates time of supply determination for RCM under GST.

Solution: Establish internal control mechanisms flagging RCM under GST supplies immediately upon receipt or invoice. Maintain a register tracking all RCM under GST transactions with relevant dates. Set system reminders for 30-day (goods) or 60-day (services) limits to ensure timely payment if other triggers haven’t occurred.

Vendor Communication

Unregistered vendors often don’t understand why registered buyers can’t simply pay them the GST amount along with supply value. Explaining RCM under GST to vendors unfamiliar with GST creates communication challenges.

Solution: Develop simple explanatory materials about RCM under GST for distribution to vendors. Explain that the law requires direct government deposit, not payment to vendor. Some businesses include RCM under GST explanations in purchase orders or vendor onboarding documents.

Penalties for Non-Compliance with RCM Under GST

GST legislation prescribes penalties for various compliance failures. RCM under GST violations attract similar consequences as other GST defaults.

Interest on Late Payment

Section 50 governs interest on delayed tax payment. Interest applies at 18% per annum from the due date until actual payment for RCM under GST.

For example, if RCM under GST time of supply occurred on March 10th but payment happens on May 20th, interest applies for 71 days on the unpaid tax amount. For ₹50,000 RCM under GST liability, interest would be approximately ₹1,750.

Tax Recovery and Penalty

Section 73 addresses recovery of tax not paid or short paid without fraud. Recovery includes:

- Tax amount

- Interest as per Section 50

- Penalty up to 10% of tax amount if paid within 30 days of notice

For RCM under GST shortfalls involving fraud or willful misstatement, Section 74 applies with harsher consequences:

- Tax amount

- Interest

Penalty up to 100% of tax amount

ITC Denial

Late RCM under GST payment risks ITC denial. While the law allows ITC claims within specified timeframes, delayed RCM under GST payment creates disputes about eligibility timing.

If RCM under GST gets paid late but within the same financial year, ITC claim typically faces no issues. However, payment in subsequent years may trigger debates about when ITC became eligible.

Impact on Vendor

Though RCM under GST places liability on recipients, non-compliance can affect vendors too. When tax authorities discover unpaid RCM under GST, they may investigate whether:

- The vendor should have registered and paid tax under forward charge

- The transaction was correctly categorized as attracting RCM under GST

- The vendor deliberately structured supplies to avoid tax

While primarily a recipient’s obligation, RCM under GST compliance failures can trigger broader investigations affecting vendors.

Prosecution in Serious Cases

Chapter XIX of the CGST Act provides for prosecution in serious violations. While RCM under GST-specific prosecution remains rare, substantial failures combined with other violations can trigger criminal consequences including:

- Imprisonment up to 5 years

- Fine

- Both imprisonment and fine

Deliberate evasion through systematic RCM under GST non-compliance, particularly involving large amounts, carries serious legal consequences beyond monetary penalties.

Vendor Communication

Unregistered vendors often don’t understand why registered buyers can’t simply pay them the GST amount along with supply value. Explaining RCM under GST to vendors unfamiliar with GST creates communication challenges.

Solution: Develop simple explanatory materials about RCM under GST for distribution to vendors. Explain that the law requires direct government deposit, not payment to vendor. Some businesses include RCM under GST explanations in purchase orders or vendor onboarding documents.

Step-by-Step Compliance Process for RCM Under GST

Following a systematic process ensures proper RCM under GST compliance.

Step 1: Identify RCM Under GST Transactions

Review all incoming supplies against notified goods and services lists. Check:

- Is the supply notified under Section 9(3)?

- Is the supplier unregistered for notified supplies under Section 9(4)?

- Does the supply come through e-commerce platforms for notified services under Section 9(5)?

Maintain a checklist accessible to procurement and accounts teams.

Step 2: Verify Supplier Status

For supplies potentially under RCM under GST:

- Obtain supplier’s GSTIN if registered

- Verify registration status on GST portal

- Determine if supplier has opted for forward charge (relevant for GTAs)

- Document verification for audit trail

Step 3: Determine Time of Supply

Calculate time of supply based on:

- For goods: Receipt date, payment date, or 31st day from invoice

- For services: Payment date or 61st day from invoice

- Book entry date if others cannot be determined

Set reminders to ensure timely compliance before automatic time of supply triggers.

Step 4: Calculate Tax Liability

Determine applicable GST rate for the supply. Calculate:

- Taxable value (excluding GST)

- CGST amount (for intra-state supplies)

- SGST/UTGST amount (for intra-state supplies)

- IGST amount (for inter-state supplies)

- Cess if applicable

Maintain calculation worksheets showing rate determination and amount computation.

Step 5: Create Self-Invoice

If supplier hasn’t issued a proper invoice (typically for unregistered suppliers):

- Generate self-invoice with all mandatory details

- Number serially in separate series from regular invoices

- Mark clearly as “Self-invoice for RCM under GST”

- Include supplier details even if incomplete

- Specify goods/services description, quantity, value

- Show calculated tax amounts

Step 6: Deposit Cash in Electronic Cash Ledger

Log into GST portal and:

- Navigate to electronic cash ledger

- Generate challan for cash deposit

- Deposit required amount covering RCM under GST liability

- Obtain challan acknowledgment

- Verify credit in cash ledger (usually within 24 hours)

Step 7: Pay RCM Under GST Liability

When filing GSTR-3B:

- Report RCM under GST liability in Table 3.1(d)

- System will debit cash ledger to discharge liability

- Ensure sufficient cash balance before filing

- Verify payment confirmation in electronic liability register

Step 8: Claim Input Tax Credit

In the same GSTR-3B:

- Report RCM under GST payment in Table 4(A)(3) as ITC

- Ensure eligibility conditions are met

- ITC will credit to electronic credit ledger

- Can be used for future GST payments

Step 9: Maintain Documentation

Organize and store:

- Original supplier invoice or self-invoice

- Payment vouchers

- Bank statements showing transactions

- Calculation worksheets

- GSTR-3B filed copies

- Supplier’s GSTR-1 (if registered and filed)

Step 10: Reconciliation

Periodically reconcile:

- RCM under GST payments made vs. actual supplies received

- ITC claimed vs. RCM under GST paid

- Supplier’s GSTR-1 Table 4B vs. your GSTR-3B reporting

- Bank statements vs. cash ledger entries

Regular reconciliation identifies discrepancies early, allowing timely correction.

Conclusion

The Reverse Charge Mechanism (RCM) under GST stands as one of the most complex components of India’s Goods and Services Tax regime. Its application spans a wide array of scenarios—ranging from agricultural commodities and professional services to property rentals and securities lending—requiring businesses to develop a deep, practical understanding and exercise meticulous compliance at every step.

RCM serves several legitimate policy objectives: securing tax from unorganized sectors, preventing revenue leakage, and simplifying compliance for government entities. However, it also places significant obligations on recipients, such as mandatory registration regardless of turnover and the requirement to pay tax in cash before claiming Input Tax Credit (ITC).

Understanding RCM under GST requires grasping multiple layers: identifying when it applies through notified lists, determining time of supply using specific rules, calculating tax liability accurately, creating proper documentation, making timely payments, and reporting correctly. Each element connects with others, where oversight in one area cascades into problems elsewhere.

Recent amendments underscore the government’s willingness to rationalize RCM provisions. For instance, the removal of sponsorship services from RCM under GST effective January 2025 reflects responsiveness to industry concerns. Nevertheless, the core provisions remain firmly in place—especially for supplies from unregistered persons, professional services, and government-related transactions.

For businesses, implementing robust internal controls is essential. Systems must identify RCM-applicable supplies at the transaction level, generate accurate documentation, ensure timely tax payments, and facilitate correct ITC claims. The cash-first nature of the mechanism necessitates careful working capital planning, even though the tax may ultimately be revenue-neutral.

Tax professionals advising clients must maintain current knowledge of notifications, circulars, and amendments. What applied yesterday may change through simple notification today. Continuous learning, regular updates monitoring, and participation in professional forums help maintain expertise in RCM under GST.

As GST matures, further refinements in RCM provisions are expected. The balance between ensuring tax compliance and minimizing taxpayer burden will continue to evolve, with greater technology integration, process simplification, and clearer guidelines likely to emerge. What remains constant is the need for thorough understanding, systematic compliance, and proactive management of RCM obligations.

Need a professional RCM Under GST Compliance & Implementation solution? TaxGroww provides complete GST Advisory Services to assist you in navigating through each of the complexities of the provisions. Contact TaxGroww today for your customized GST solution that meets your unique business needs. We can turn your RCM Under GST Compliance into a strategic advantage rather than an obligation.