Table of Contents

Introduction

Receiving gifts brings joy, but understanding their tax implications often creates confusion among taxpayers. Whether it’s cash from your parents for a house purchase, jewelry from in-laws during marriage, or property gifted by a close friend, each transaction carries specific tax consequences under Indian Income Tax law.

Income Tax on Gifts has evolved significantly over the years, with the Income Tax Act, 1961 providing detailed provisions under Section 56(2)(x) that determine when gifts become taxable income. Many taxpayers unknowingly face tax liabilities or miss legitimate exemptions simply because they lack clarity about these complex provisions.

This comprehensive guide demystifies the intricate world of gift taxation, covering everything from basic definitions to advanced compliance requirements. We’ll explore how the relationship between donor and recipient affects tax liability, examine various types of gifts and their specific treatment, and provide practical insights for optimal tax planning.

Understanding Framework of Income Tax on Gifts

Definition of Gift Under Income Tax Act

Under Section 56(2)(x) of the Income Tax Act, 1961, a gift refers to any sum of money, moveable property, or immovable property received without consideration or for inadequate consideration. The provision specifically targets situations where the recipient receives value without providing equivalent compensation.

The fundamental principle underlying gift taxation is that any benefit received by an individual should be subject to tax, preventing tax avoidance through artificial transactions disguised as gifts. However, the law recognizes genuine familial transactions and provides specific exemptions to avoid taxing natural family support systems.

Taxability in Recipient's Hands

Unlike many other jurisdictions, India follows the principle of taxing gifts in the hands of the recipient rather than the donor. This means the person receiving the gift bears the tax liability, while the donor generally faces no tax consequences for making the gift.

The taxable gift is classified as “Income from Other Sources” and added to the recipient’s total income for the relevant assessment year. This classification subjects the gift income to the recipient’s applicable tax slab rates, making it crucial to consider the overall tax impact when planning gift transactions.

Section 56(2)(x) Provisions Explained

Scope and Application

Section 56(2)(x) encompasses three distinct categories of gifts:

- Sum of money received without consideration

- Moveable property received without consideration or inadequate consideration

- Immovable property received without consideration or inadequate consideration

Each category has specific threshold limits and valuation methods that determine taxability. The provision applies to individuals and Hindu Undivided Families (HUFs), making it relevant for most personal gift transactions.

Threshold Limits

The law provides a universal exemption threshold of ₹50,000 per financial year for aggregate gifts received from non-relatives. This means gifts totaling ₹50,000 or less from non-relatives remain completely exempt from tax, regardless of the number of donors or occasions.

For gifts exceeding this threshold, the entire amount becomes taxable, not just the excess over ₹50,000. This “all or nothing” approach makes careful planning essential when gift values approach the threshold limit.

Exemptions for Gifts from Relatives

Definition of Relative

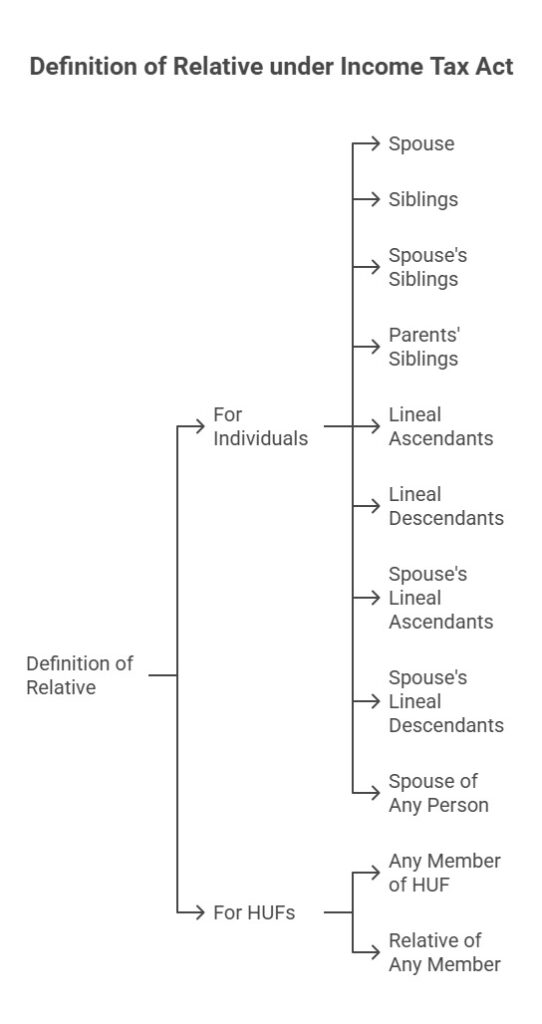

The Income Tax Act provides an exhaustive definition of “relative” under Section 56(2)(x), covering:

For Individuals:

- Spouse of the individual

- Brother or sister of the individual

- Brother or sister of the spouse of the individual

- Brother or sister of either of the parents of the individual

- Any lineal ascendant or descendant of the individual

- Any lineal ascendant or descendant of the spouse of the individual

- Spouse of any person mentioned above

For HUFs:

- Any member of the HUF

- Relative of any member of the HUF as defined above

Complete Exemption for Relative Gifts

Gifts received from relatives enjoy complete exemption from income tax, irrespective of the amount or nature of the gift. This exemption recognizes the natural flow of wealth within families and ensures that genuine family support systems remain untaxed.

The exemption applies to all forms of gifts – cash, moveable property, immovable property, and even inadequate consideration transactions between relatives. This comprehensive coverage makes relative gifts one of the most effective tax planning tools available.

Importance of Establishing Relationship

- Marriage certificates

- Birth certificates

- Family records

- Ration cards

- Passport details showing family members

- Affidavits with supporting documents

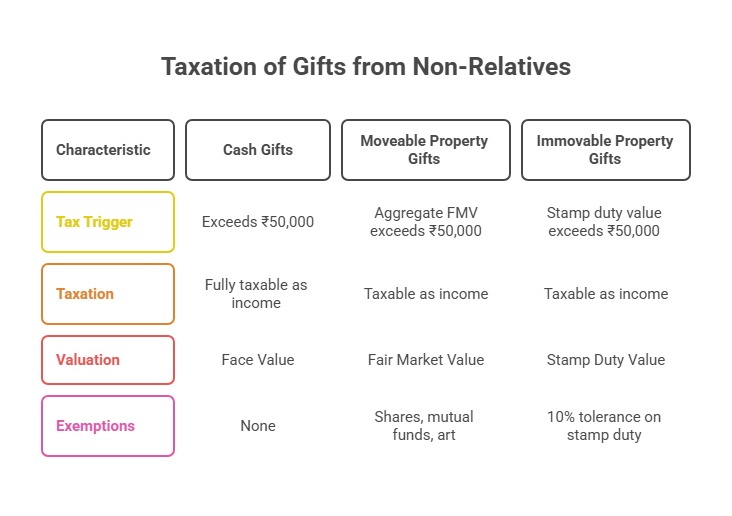

Taxation of Gifts from Non-Relatives

Cash Gifts

Cash gifts from non-relatives exceeding ₹50,000 in aggregate during a financial year become fully taxable as income from other sources. The timing of receipt determines the relevant assessment year, making it important to track gift receipts across financial years.

For tax purposes, cash includes:

- Physical currency

- Bank drafts

- Cheques

- Digital payments

- Cryptocurrencies (as per current interpretation)

Moveable Property Gifts

Moveable property gifts from non-relatives become taxable when the aggregate fair market value exceeds ₹50,000 per financial year. The fair market value is determined as of the date of receipt, requiring professional valuation for significant items.

Exempt Moveable Properties:

- Shares and securities listed on recognized stock exchanges

- Units of mutual funds

- Units of specified schemes (as notified)

- Archaeological collections, paintings, sculptures, drawings, books, dresses, jewelry, and other personal effects

Immovable Property Gifts

Immovable property gifts from non-relatives are taxable based on their stamp duty value if it exceeds ₹50,000. The stamp duty value, as adopted by the registration authority, serves as the benchmark for taxation purposes.

However, a practical relaxation allows up to 10% tolerance if the actual consideration paid exceeds 90% of the stamp duty value. This provision prevents taxation of minor valuation differences while maintaining the integrity of the gift taxation framework.

GST Return Filing Requirements

GSTR-8 Filing Requirements

E-commerce operators must file Form GSTR-8 monthly, reporting TCS collections and supplier transaction details. This return serves as the primary compliance document for TCS operations and requires comprehensive transaction reporting.

Filing Frequency: Monthly filing by 10th of succeeding month, ensuring timely compliance with GST compliance for e-commerce operators requirements.

Information Requirements:

- Details of all suppliers transacting through the platform

- TCS collected and deposited amounts

- Supply-wise transaction details

- Refund and adjustment particulars

Trust and Registered Societies

Gifts received from trusts or institutions registered under Section 12AA, political parties, and certain other specified entities enjoy exemption from gift taxation. This provision ensures that charitable receipts and institutional support remain outside the tax net.

Local Authorities

Gifts from local authorities, as defined under relevant laws, are exempt from taxation. This includes gifts from municipal corporations, panchayats, and other governmental bodies.

Valuation Aspects

Fair Market Value Determination

- Current market conditions

- Property condition and age

- Comparable transactions

- Professional valuations where necessary

Stamp Duty Valuation

For immovable property, stamp duty value adopted by the registration authority serves as the benchmark. This value is generally higher than market value, ensuring adequate tax coverage while providing certainty in valuation.

Consideration Analysis

When property is received for consideration, the difference between fair market value and actual consideration paid determines taxability. If this difference exceeds ₹50,000, it becomes taxable as a gift.

Documentation Requirements

Essential Records

Proper documentation forms the backbone of gift taxation compliance:

For All Gifts:

- Gift deed or document evidencing the transaction

- Relationship proof (for relative exemption claims)

- Valuation certificates for significant gifts

- Bank statements showing receipt

- Identity documents of donor and recipient

For Property Gifts:

- Registration documents

- Title deeds

- Valuation reports

- Stamp duty payment receipts

- Survey settlement documents

Maintaining Gift Registers

- Date of receipt

- Donor details and relationship

- Nature and value of gift

- Supporting documents

- Tax treatment applied

Tax Planning Strategies

Timing Considerations

- Spreading large gifts across financial years to utilize annual exemptions

- Coordinating with income levels to manage tax slab implications

- Planning around marriage and other exempt occasions

Structural Planning

- Gifts routed through eligible relatives

- Proper documentation of family relationships

- Creating legitimate consideration arrangements

Investment Planning

- Listed securities instead of cash

- Exempt personal effects instead of taxable property

- Utilizing trust structures for larger transfers

Compliance and Reporting

ITR Disclosure Requirements

- Total gift income received

- Details of major donors

- Basis of taxation applied

- Exemptions claimed

TDS Implications

Currently, no TDS provisions apply to gift receipts. However, recipients must ensure proper disclosure and tax payment through advance tax or self-assessment tax mechanisms.

Assessment Risks

- Relationship proof disputes

- Valuation challenges

- Timing of receipt questions

- Source verification by donors

Practical Examples and Case Studies

Case Study 1: Marriage Gifts

Priya receives ₹5,00,000 cash from various relatives and ₹2,00,000 from friends during her marriage. The entire amount remains exempt under marriage occasion exemption, demonstrating the power of timing-based exemptions.

Case Study 2: Property Gifts

Raj receives a plot worth ₹25,00,000 from his uncle (father’s brother). Being a relative transaction, the entire gift remains exempt regardless of value, highlighting the importance of family relationship planning.

Case Study 3: Mixed Gifts

Sunita receives ₹30,000 from a colleague and ₹25,000 from a neighbor during the financial year. The total ₹55,000 from non-relatives exceeds the ₹50,000 threshold, making the entire amount taxable.

Common Mistakes to Avoid

Documentation Failures

- Inadequate relationship proof maintenance

- Missing gift deeds or transaction records

- Improper valuation documentation

- Timing evidence gaps

Planning Errors

- Ignoring aggregate thresholds

- Misunderstanding exemption scopes

- Poor timing coordination

- Inadequate compliance preparation

Assessment Challenges

- Inability to substantiate claims

- Valuation disputes with authorities

- Source verification failures

- Penalty exposures for non-compliance

Professional Advice and Best Practices

When to Consult Professionals

- Large value transfers

- Multiple donor situations

- Property gift transactions

- Cross-border gift implications

- Assessment proceedings

Best Practice Framework

- Regular compliance reviews

- Documentation maintenance systems

- Professional relationship management

- Proactive tax planning integration

Conclusion

Understanding gift taxation under Indian Income Tax law requires careful attention to relationship definitions, valuation methods, and compliance requirements. The distinction between relative and non-relative gifts, combined with various exemptions and threshold limits, creates opportunities for effective tax planning while demanding meticulous documentation and compliance.

Success in gift taxation matters depends on proactive planning, proper documentation, and professional guidance for complex situations. By understanding these provisions thoroughly and implementing appropriate strategies, taxpayers can optimize their gift-related tax implications while ensuring full compliance with regulatory requirements.

For comprehensive tax planning and compliance support, consider consulting with professional tax advisors who can provide personalized guidance based on your specific circumstances. At Taxgroww , we specialize in helping individuals and families navigate complex tax situations with confidence and expertise

Frequently Asked Questions (FAQs)

1. What is the maximum amount I can receive as a gift from non-relatives without paying tax?

You can receive up to ₹50,000 in aggregate from all non-relatives during a financial year without any tax liability. If the total exceeds ₹50,000, the entire amount becomes taxable, not just the excess.

2. Are gifts from relatives completely tax-free regardless of the amount?

Yes, gifts from relatives as defined under Section 56(2)(x) are completely exempt from income tax, irrespective of the amount or nature of the gift. This includes cash, property, jewelry, and all other forms of gifts.

3. How do I prove that the gift was received from a relative?

You need to maintain proper documentation such as marriage certificates, birth certificates, family records, ration cards, passport details, or affidavits with supporting documents to establish the relationship with the donor.

4. What happens if I receive gifts worth ₹60,000 from non-relatives during the year?

The entire ₹60,000 becomes taxable as “Income from Other Sources” since it exceeds the ₹50,000 threshold. You cannot claim exemption for the first ₹50,000 – it’s an all-or-nothing provision.

5. Are marriage gifts taxable even if received from non-relatives?

No, gifts received on the occasion of marriage are completely exempt from income tax under Section 56(2)(vii), regardless of who gives them. This exemption covers all marriage-related gifts from any donor.

6. How is the value of jewelry or property gifts determined for tax purposes?

For moveable property like jewelry, the fair market value on the date of receipt is considered. For immovable property, the stamp duty value adopted by the registration authority is used for taxation purposes.

7. Can I receive shares or mutual fund units as gifts without tax implications?

Listed shares, securities, and mutual fund units are exempt from gift taxation when received from non-relatives, provided they are traded on recognized stock exchanges or are specified schemes.

8. What if I receive property for partial consideration from a non-relative?

If the difference between fair market value and actual consideration paid exceeds ₹50,000, that difference becomes taxable as a gift. A 10% tolerance is allowed for immovable property transactions.

9. Do I need to report gifts from relatives in my income tax return?

Gifts from relatives are exempt and generally don’t need to be reported. However, if you claim any exemption or deduction related to the gift, proper disclosure might be required for transparency.

10. Can I give gifts without any tax liability on my part?

Generally, there’s no tax liability on the donor (person giving the gift) in India. The tax responsibility lies with the recipient. However, ensure proper documentation to avoid future complications.

11. What constitutes 'occasion of marriage' for gift tax exemption?

The occasion of marriage includes gifts received during the marriage ceremony and gifts given in reasonable connection with the marriage, which could include gifts received before or shortly after the actual ceremony.

12. Are gifts received from trusts or NGOs taxable?

Gifts from trusts registered under Section 12AA, political parties, and certain other specified institutions are exempt from gift taxation, provided they meet the specified criteria under the Income Tax Act.

13. How should I maintain records for gift transactions?

Maintain detailed records including gift deeds, donor details, relationship proof, valuation certificates, bank statements, and any other supporting documents. Consider maintaining a gift register for systematic record-keeping.

14. Can I spread a large gift across multiple years to reduce tax impact?

Yes, if structured properly, spreading gifts across financial years can help utilize the annual ₹50,000 exemption limit for non-relative gifts and manage your overall tax liability effectively.

15. What happens if I cannot prove the relationship with the donor?

If you cannot establish the relationship through proper documentation, the gift will be treated as received from a non-relative, making it subject to the ₹50,000 threshold limit and potential taxation.

16. Are gifts received from foreign relatives exempt from tax?

Yes, the relative exemption applies regardless of the donor’s location. However, you must still comply with foreign exchange regulations (FEMA) and maintain proper documentation to establish the relationship.

17. Is there any limit on the number of gift transactions in a year?

There’s no limit on the number of gift transactions. However, for non-relatives, the aggregate value matters for the ₹50,000 exemption threshold. Each transaction must be properly documented regardless of value.

18. What are the penalties for not reporting taxable gifts?

Non-reporting of taxable gifts can result in tax liability with interest, penalties under Section 270A for underreporting of income, and potential prosecution in cases of deliberate tax evasion. Proper compliance is essential to avoid these consequences.

whoah this weblog is magnificent i really like studying your posts. Keep up the good work! You recognize, lots of individuals are hunting around for this info, you could help them greatly.

I am glad to be a visitant of this double dyed blog! , appreciate it for this rare info ! .

I really like your writing style, excellent information, thankyou for putting up : D.

I got what you mean ,saved to bookmarks, very nice site.

There is noticeably a bundle to know about this. I assume you made certain nice points in features also.

Sir,

In a partnership firm consisting of husband and wife as partners, they intend to gift the firm’s property to their major son. Since a partnership is legally regarded as an extension of its partners, kindly clarify whether such a gift would be taxable in the hands of the firm. Thanks in advance