Table of Contents

Introduction

Have you made mistakes in filing your ITR and wondering how to correct them? Every taxpayer encounters situations where errors surface after filing their income tax return. Whether it’s unreported income, miscalculated deductions, or simple computational mistakes, the Income Tax Act provides specific mechanisms to address these issues. Understanding when to revise income tax return versus when to seek rectification can save you from penalties and ensure proper tax compliance.

The Income Tax Department acknowledges that taxpayers may discover omissions or errors after filing their returns. This is precisely why the law provides two distinct correction mechanisms – revision under Section 139(5) and rectification under Section 154. However, the confusion between these two procedures often leads taxpayers down the wrong path, potentially creating additional complications.

The key lies in understanding that while both procedures serve to correct mistakes, they address fundamentally different types of errors and operate under separate legal frameworks. Your choice between revise income tax return and rectification depends on the nature of your error, timing constraints, and who can initiate the correction process.

Understanding Income Tax Return Revision

What is ITR Revision?

Income Tax Return revision is a process that allows taxpayers to correct errors or omissions in their originally filed return by filing a fresh return. Under Section 139(5) of the Income Tax Act, 1961, any taxpayer who discovers mistakes in their filed return can submit a revised return to replace the original one.

The revision process essentially treats the new return as the final and correct version, superseding all previous submissions. This mechanism acknowledges that taxpayers might overlook certain income sources, claim incorrect deductions, or make computational errors during the initial filing process.

Legal Framework for Revision

Section 139(5) of the Income Tax Act states that if any person, having furnished a return under sub-section (1) or sub-section (4), discovers any omission or any wrong statement therein, he may furnish a revised return at any time before the expiry of one year from the end of the relevant assessment year or before the completion of the assessment, whichever is earlier.

This provision underwent significant changes with the Finance Act 2017, which extended the time limit for filing revised returns from the earlier deadline of March 31st of the assessment year to December 31st of the assessment year. This change provided taxpayers with additional time to identify and correct errors.

When Can You Revise ITR?

You can revise income tax return in specific circumstances that involve substantial changes to your tax position:

Omission of Income Sources: When you discover income that wasn’t included in your original return – interest from forgotten bank accounts, dividend income, rental income, or capital gains that were inadvertently omitted.

Incorrect Deduction Claims: If you realize certain deductions were claimed incorrectly, or you’re entitled to additional deductions under sections like 80C, 80D, or other applicable provisions that weren’t initially claimed.

Computational Errors in Tax Calculation: When there are significant errors in tax computation, including incorrect application of tax rates, wrong calculation of advance tax credits, or TDS mismatches.

Change in Tax Regime: If you need to switch between old and new tax regimes (subject to restrictions for business income taxpayers).

Wrong ITR Form Selection: When you initially filed using an incorrect ITR form – for instance, filing ITR-1 when you should have used ITR-2 due to capital gains or other income sources.

Time Limit for Revision

The time limit for filing a revised income tax return is crucial to understand. As per Section 139(5), you can file a revised return:

- Before December 31st of the relevant assessment year, OR

- Before completion of assessment proceedings, whichever is earlier

For Assessment Year 2025-26 (Financial Year 2024-25), the last date for filing a revised return is December 31, 2025, provided the assessment hasn’t been completed before this date.

Important Note: Even belated returns (filed after the due date) can be revised within the same timeframe. This provision was introduced from FY 2016-17, expanding the scope of revision to include belated filings.

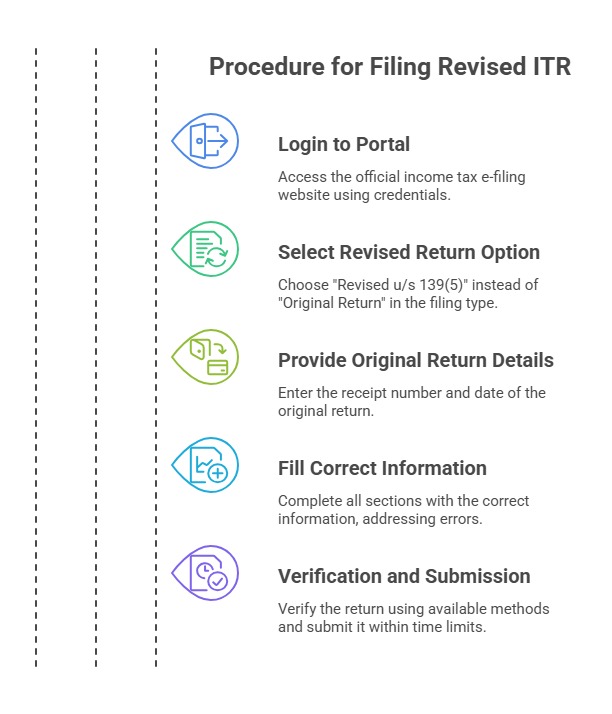

Procedure for Filing Revised ITR

Filing a revised return follows a systematic process:

Step 1: Login to Income Tax E-filing Portal Access the official income tax e-filing website using your credentials.

Step 2: Select Revised Return Option While filing the return, select “Revised u/s 139(5)” instead of “Original Return” in the filing type.

Step 3: Provide Original Return Details Enter the receipt number and date of the original return that you’re revising.

Step 4: Fill Correct Information Complete all sections with the correct information, ensuring all errors from the original return are addressed.

Step 5: Verification and Submission Verify the return using available methods and submit it within the prescribed time limits.

Understanding Rectification of ITR

What is Rectification?

Rectification is a process available under Section 154 of the Income Tax Act that allows correction of apparent errors or omissions in assessment orders, returns, or other documents. Unlike revision, rectification can be initiated by either the taxpayer or the Assessing Officer.

The concept of rectification is based on the principle that obvious mistakes should be correctable without going through the elaborate process of appeal or revision. These are typically errors that are apparent from the record and don’t require detailed investigation or interpretation of law.

Legal Provisions for Rectification

Section 154 of the Income Tax Act provides the legal framework for rectification. The section states that the Assessing Officer may, either suo moto or on an application by the assessee, amend any order passed by him under the provisions of this Act, so as to rectify any mistake apparent from the record.

The Supreme Court in the case of T.S. Balaram vs. Volkart Brothers has established that a mistake apparent from record means “an obvious and patent mistake and not something which can be established by a long drawn process of reasoning on points on which there may conceivably be two opinions.”

Types of Errors Covered Under Rectification

Rectification under Section 154 covers specific types of errors that are apparent from the record:

Arithmetical Mistakes: Simple calculation errors, incorrect addition or subtraction, wrong totaling of figures, or basic computational mistakes.

Clerical Errors: Typographical mistakes, wrong entry of names, addresses, PAN numbers, or similar clerical inaccuracies.

Tax Credit Mismatches: Incorrect TDS credits, advance tax credits, or self-assessment tax entries that don’t match with the department’s records.

Schedule-Related Errors: Mistakes in salary schedules, bank interest schedules, or other pre-filled schedules that contain obvious errors.

Apparent Factual Errors: Wrong dates, incorrect figure entries, or similar factual mistakes that are evident from supporting documents without requiring interpretation.

Rectification Process and Methods

The rectification process can be initiated through multiple methods based on the type of error:

Method 1: Reprocess the Return This is the simplest method where you request the department to reprocess your return without making any changes. This is suitable when the error is purely computational.

Method 2: Tax Credit Mismatch Correction This method allows editing of specific schedules like:

- Tax Payment and Verification Details

- TDS Details (Salary, Other than Salary)

- Advance Tax and Self-Assessment Tax Details

- Tax Relief Details

Method 3: Upload Rectified JSON/XML File For more complex rectifications, you can download your original return data, make corrections using the offline utility, and upload the rectified file. However, this method has restrictions – you cannot add new income sources or claim additional deductions.

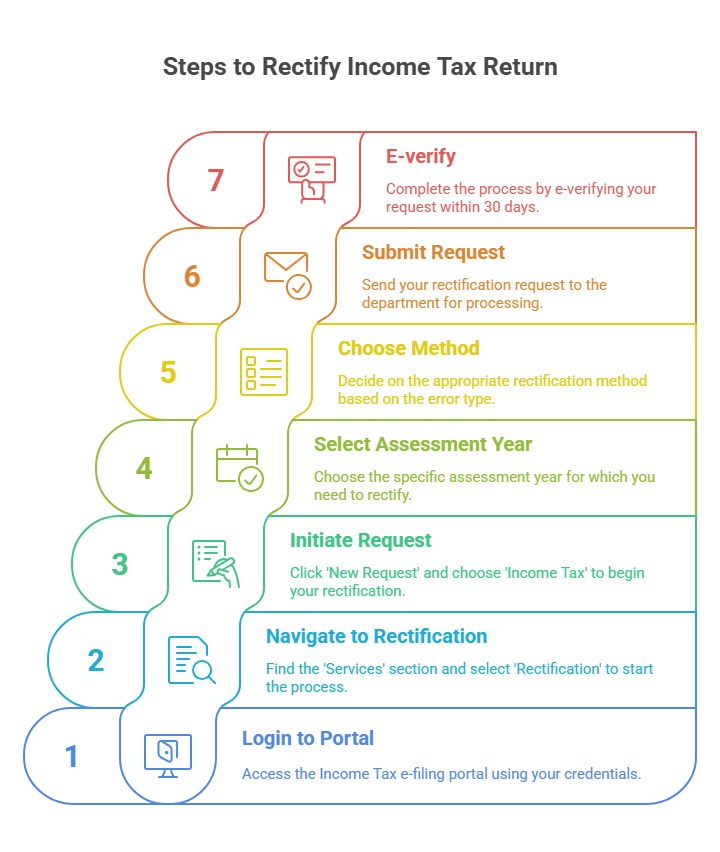

Online Rectification Steps:

- Login to the Income Tax e-filing portal

- Navigate to ‘Services’ → ‘Rectification’

- Click ‘New Request’ and select ‘Income Tax’

- Choose the relevant assessment year

- Select appropriate rectification method

- Submit the rectification request

- E-verify the rectification within 30 days

Time Limit for Rectification

The time limit for rectification is different from revision:

For Assessing Officer: Four years from the end of the financial year in which the order sought to be rectified was passed.

For Taxpayer: Four years from the end of the financial year in which the order was passed, but the application must be made to the officer who passed the original order.

These time limits are much longer than revision periods, reflecting the fact that rectification addresses fundamental errors that might take time to discover.

Key Differences between Revision and Rectification

Understanding the differences between revise income tax return and rectification is crucial for taxpayers to choose the appropriate remedy:

Nature of Errors

Revision: Covers substantial errors, omissions of income, incorrect deductions, and matters requiring judgment or interpretation of law.

Rectification: Limited to apparent errors, clerical mistakes, and arithmetical errors that are obvious from the record.

Initiating Authority

Revision: Can only be initiated by the taxpayer who filed the original return.

Rectification: Can be initiated by either the taxpayer through application or by the Assessing Officer suo moto.

Time Limits

Revision: One year from the end of assessment year or before completion of assessment, whichever is earlier.

Rectification: Four years from the end of the financial year in which the order was passed.

Legal Framework

Revision: Governed by Section 139(5) of the Income Tax Act.

Rectification: Governed by Section 154 of the Income Tax Act.

Scope of Changes

Revision: Allows comprehensive changes to the return, including addition of new income sources, modification of deductions, and change in tax calculations.

Rectification: Limited to correction of apparent mistakes without changing the fundamental nature of assessment.

Documentation Required

Revision: Requires filing a complete fresh return with all supporting documents.

Rectification: Requires only an application pointing out the specific error with supporting evidence.

Detailed Comparison Table

Aspect | Revision u/s 139(5) | Rectification u/s 154 |

Legal Basis | Section 139(5) of Income Tax Act | Section 154 of Income Tax Act |

Who Can Initiate | Only the taxpayer | Taxpayer or Assessing Officer |

Type of Errors | Substantial errors, omissions, wrong claims | Apparent errors, clerical mistakes, computational errors |

Time Limit | December 31 of AY or before assessment completion | 4 years from end of financial year |

Process | File complete revised return | Submit rectification request online |

Fees | No additional fees | No fees for rectification |

Impact | Replaces original return entirely | Corrects specific errors only |

New Deductions | Can claim additional deductions | Cannot claim new deductions |

Income Addition | Can add omitted income sources | Cannot add new income sources |

Form Change | Can change ITR form if needed | Cannot change ITR form |

Verification Required | Must be e-verified within 30 days | Must be e-verified within 30 days |

Processing Method | Complete return processing | Targeted error correction |

Practical Scenarios and Applications

When to Choose Revision

Scenario 1: Omitted Capital Gains If you forgot to report capital gains from sale of mutual funds worth ₹3,00,000, this requires revision as it’s a substantial income omission affecting your total taxable income.

Scenario 2: Missed Section 80C Deduction When you initially claimed ₹1,00,000 under Section 80C but later realized you could claim ₹1,50,000 due to additional ELSS investments, this needs revision.

Scenario 3: Tax Regime Change If you want to switch from new tax regime to old tax regime (applicable for salary income taxpayers), this requires filing a revised income tax return.

Scenario 4: Wrong ITR Form Filing ITR-1 when you should have filed ITR-2 due to capital gains or house property income requires revision with the correct form.

When to Choose Rectification

Scenario 1: TDS Credit Mismatch If your Form 16 shows TDS of ₹25,000 but you entered ₹2,500 in your return due to a typing error, this apparent mistake can be rectified.

Scenario 2: Incorrect Bank Interest When the pre-filled data shows bank interest of ₹15,000 but the correct amount is ₹18,000 based on your bank statements, this can be rectified.

Scenario 3: Wrong Tax Payment Details If you entered wrong challan details or advance tax amounts that don’t match department records, rectification is the appropriate remedy.

Scenario 4: Computational Errors Simple addition errors in salary schedules or wrong calculation of tax liability due to arithmetic mistakes can be corrected through rectification.

Common Mistakes to Avoid

Revision Mistakes

Missing Documentation: Failing to maintain proper documentation for revised claims can lead to scrutiny and disallowance.

Exceeding Time Limits: Many taxpayers miss the one-year deadline, making revision impossible and forcing them to live with errors.

Incomplete Correction: Some taxpayers correct one error but miss others, necessitating multiple revisions which can trigger scrutiny.

Wrong Form Selection: Using incorrect ITR form during revision can create additional complications.

Rectification Mistakes

Requesting Rectification for Complex Issues: Trying to rectify matters that require interpretation or judgment, which should be addressed through revision or appeal.

Inadequate Supporting Evidence: Failing to provide clear evidence of the apparent error can lead to rejection of rectification application.

Delayed Applications: Although the time limit is four years, delayed applications might face additional scrutiny.

Impact on Tax Liability and Refunds

Revision Impact

When you file a revised income tax return, the impact on tax liability can be significant:

Additional Tax Liability: If the revision results in higher taxable income, you’ll need to pay additional tax along with applicable interest under Section 234A, 234B, or 234C.

Refund Claims: If revision results in excess tax payment, you can claim refund, but processing might take longer than normal returns.

Interest Implications: Interest calculations change based on the revised figures, affecting the final tax liability.

Rectification Impact

Rectification typically has minimal impact on tax liability since it addresses apparent errors:

Minor Adjustments: Usually results in small adjustments to tax liability or refund amounts.

No Interest Implications: Generally doesn’t affect interest calculations unless the error was in computation of interest itself.

Quick Processing: Rectification orders are typically processed faster than revision cases.

Important Restrictions and Limitations

Revision Restrictions

Cannot Revise After Assessment: Once the assessment proceedings are completed, you cannot file a revised income tax return even if the December 31st deadline hasn’t passed.

Original Return Must Be Filed: You can only revise returns that were originally filed within the due date or as belated returns. However, belated returns can also be revised within the same timeframe.

E-verification Mandatory: Both original and revised returns must be e-verified within 30 days of filing for the revision to be valid.

Multiple Revisions Allowed: There’s no limit on the number of times you can revise, but each subsequent revision replaces the previous one entirely.

Rectification Restrictions

No New Claims: You cannot claim additional deductions, exemptions, or add new income sources through rectification. These require revision.

No Structural Changes: Cannot change ITR forms, tax regimes, or make fundamental changes to the return structure.

Return Must Be Processed: Rectification can only be filed for returns that have already been processed by the Central Processing Centre (CPC), Bangalore.

Limited to Apparent Errors: Only mistakes that are obvious from the record without requiring interpretation or investigation can be rectified.

Recent Updates and Changes

Finance Act 2017 Modifications

The Finance Act 2017 brought significant changes to the revision framework:

Extended Deadline: The deadline for filing revised returns was extended from March 31st to December 31st of the assessment year, providing taxpayers with additional nine months.

Belated Return Revision: The provision allowing revision of belated returns was retained, ensuring comprehensive error correction opportunities.

Digital Processing Enhancements

Recent technological improvements have streamlined both processes:

Automated Rectification: Simple computational errors and TDS mismatches are often automatically identified and corrected by the system.

Online Tracking: Taxpayers can track the status of both revision and rectification requests through the e-filing portal.

Faster Processing: The Central Processing Centre has reduced processing times for both revisions and rectifications through automation.

Best Practices for Taxpayers

Before Filing Original Return

Thorough Review: Carefully review all documents, calculations, and entries before filing the original return.

Professional Consultation: Consider consulting tax professionals for complex cases to minimize errors.

Document Maintenance: Maintain proper documentation for all claims and income sources.

When Errors Are Discovered

Quick Assessment: Immediately assess whether the error requires revision or can be rectified.

Time Consideration: Consider time limits while deciding on the course of action.

Professional Advice: Seek professional guidance for complex errors or interpretation issues.

During Revision/Rectification Process

Complete Information: Provide complete and accurate information in revised returns or rectification applications.

Supporting Documents: Attach all necessary supporting documents to avoid queries.

Follow-up: Regularly follow up on the status of your application.

Final Thoughts

Understanding the distinction between revise income tax return and rectification procedures is fundamental for effective tax compliance management. Both mechanisms serve distinct purposes within the Income Tax framework – revision addresses substantial errors and omissions that affect your tax liability, while rectification handles apparent mistakes and clerical errors that don’t require complex interpretation.

The choice between these two correction methods depends on the nature of your error, timing considerations, and the scope of changes required. When you discover significant omissions like unreported income sources or missed deductions, revise income tax return under Section 139(5) is your appropriate remedy. For simple computational mistakes, TDS mismatches, or clerical errors, rectification under Section 154 provides a quicker solution.

Time limits play a crucial role in your decision-making process. While you have until December 31st of the assessment year to revise income tax return, rectification requests can be submitted up to four years from the relevant financial year. However, remember that rectification is limited to apparent errors and cannot be used to make substantial changes to your tax position.

The Income Tax Department’s digital initiatives have made both processes more accessible and efficient. Whether you choose revision or rectification, ensure that you e-verify your submission within 30 days and maintain proper documentation to support your corrections.

For expert guidance on income tax return revision and rectification procedures, professional consultation can help you navigate complex tax situations effectively. TaxGroww offers comprehensive tax advisory services to help you make informed decisions about error corrections, ensuring compliance while optimizing your tax position. Our experienced professionals can guide you through the intricacies of both revision and rectification processes, helping you choose the right approach for your specific situation and ensuring that your tax affairs remain in perfect order.