Table of Contents

Introduction

The Income Tax Department dropped some major changes for ITR-1 and ITR-4 additional disclosure requirements for AY 2025-26. And honestly? It caught many of us off guard.

If you’re filing under the old tax regime, these ITR-1 and ITR-4 additional disclosure requirements for AY 2025-26 will need you to dig deeper into your documentation than ever before. Gone are the days when you could simply mention exemption amounts and move on. The department wants details. Lots of them.

I’ve been reviewing these ITR-1 and ITR-4 additional disclosure requirements for AY 2025-26, and while some make perfect sense from a verification standpoint, others feel like they’re adding complexity where simplicity once existed. But then again, maybe that’s the point.

What's Really Changed Here?

The revised forms aren’t just asking for more information—they’re asking for the right information. Understanding these ITR-1 and ITR-4 additional disclosure requirements for AY 2025-26 makes the difference between smooth filing and assessment complications.

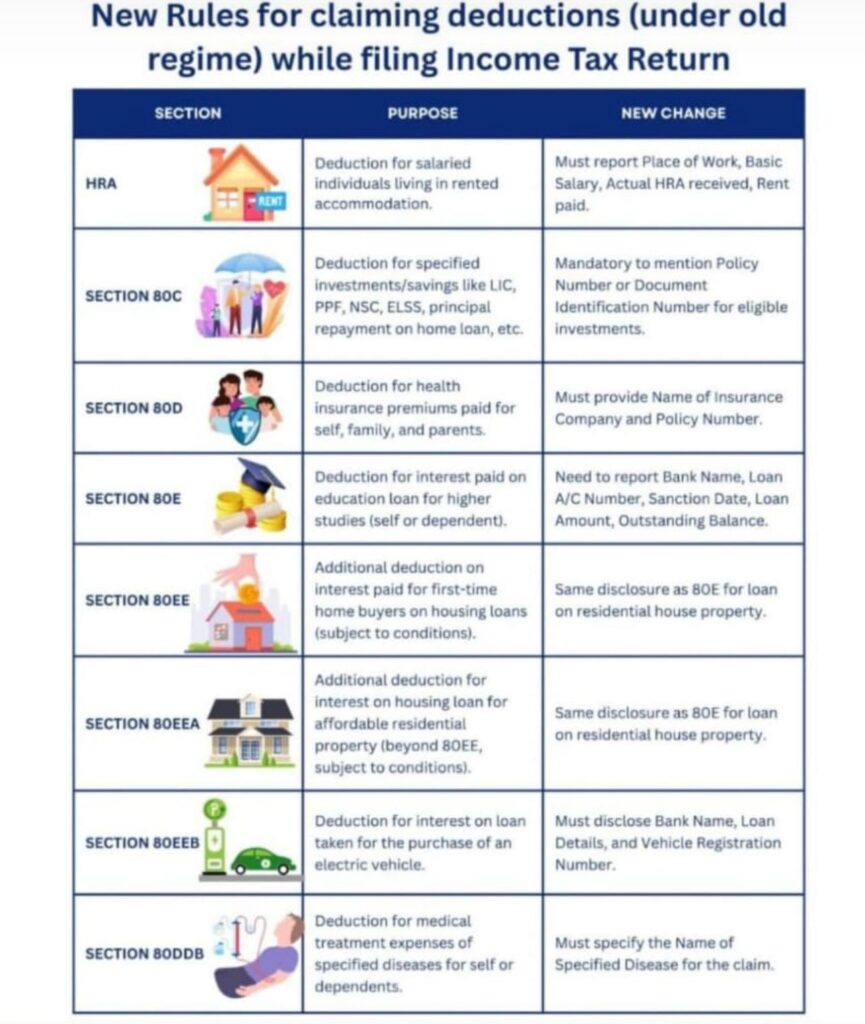

Think of it this way: earlier, you declared your HRA exemption amount. Now you need to show your work. Every step of it.

HRA Exemption under Section 10(13A): Core ITR-1 and ITR-4 additional disclosure requirements for AY 2025-26

You’ll need to provide:

Place of Work – Not just the city, but the actual workplace address. Makes sense when you think about it—metro vs non-metro calculations depend on where you actually work, not where your company is headquartered.

Actual HRA Received – This one’s straightforward. The total HRA component from your salary slips.

Actual Rent Paid – Here’s where it gets tricky for some people. If your rent varied during the year, you’ll need to calculate the total. No approximations.

Basic Salary and Dearness Allowance – Segregated amounts. Not combined figures.

Metro/Non-Metro Percentage – The 50% or 40% calculation basis. This ties back to your place of work.

The calculation methodology under Section 10(13A) hasn’t changed, which is somewhat reassuring. But the documentation requirements? That’s a different story entirely.

I’ve seen cases where people claimed HRA exemption based on rough estimates or outdated rent agreements. That approach won’t work anymore. The form essentially cross-checks your claim against multiple data points.

Section 80C: Critical Component of ITR-1 and ITR-4 additional disclosure requirements for AY 2025-26

Section 80C deductions represent a major aspect of ITR-1 and ITR-4 additional disclosure requirements for AY 2025-26, now requiring what I’d call “forensic-level” documentation. Though maybe that’s an exaggeration. Or maybe it isn’t.

For PPF contributions, you need:

- Complete PPF account number (all 14 digits)

- Bank or post office branch details

- Receipt numbers for each contribution

Life insurance premiums require:

- Policy numbers

- Insurance company names

- Policy type classifications

The challenge here isn’t just gathering information—it’s maintaining it throughout the year. Most people don’t think about organizing tax documents until March rolls around. That strategy needs to change.

Tax-saving fixed deposits add another layer. Bank names, branch details, receipt numbers, maturity dates. It’s comprehensive, though I suppose it needed to be.

Medical Insurance under Section 80D: Essential ITR-1 and ITR-4 additional disclosure requirements for AY 2025-26

Health insurance deductions now demand institutional information that goes beyond premium amounts under the ITR-1 and ITR-4 additional disclosure requirements for AY 2025-26. The forms want to know exactly who you’re insured with and under what policy.

Insurance company name—complete registered name, not abbreviated versions. Policy numbers in full. Premium payment modes. Beneficiary specifications.

For senior citizen parents’ coverage, the requirements extend further. Age verification documents might be needed during assessment proceedings. Though the forms don’t explicitly state this, it’s implied in the enhanced scrutiny approach.

The preventive health check-up component under Section 80D also falls under this detailed reporting requirement. Receipts, service provider details, family member specifications—all of it matters now.

Education Loan Interest: Section 80E Documentation

This section presents interesting challenges within the broader ITR-1 and ITR-4 additional disclosure requirements for AY 2025-26 framework. Education loan interest deductions now require comprehensive loan documentation that many borrowers might not have readily available.

Lender institution names—complete, not abbreviated. Branch details where the loan was sanctioned. Loan account numbers in full. Original sanction dates. Total sanctioned amounts. Outstanding balances as of March 31st.

The documentation continues throughout the loan repayment period. Which makes sense, considering the deduction continues until full repayment. But it also means maintaining loan statements year after year.

Students who’ve taken education loans and parents who’ve co-borrowed need to coordinate documentation. Sometimes the borrower isn’t the one claiming the deduction—family dynamics can complicate tax planning.

Home Loan Interest: Sections 80EE and 80EEA

First-time home buyers claiming interest deductions face similar documentation requirements. Though the sections differ—80EE for certain loan amounts and property values, 80EEA for affordable housing—the documentation approach remains consistent.

Financial institution details, complete with branch information. Loan account numbers. Sanction dates. Sanctioned amounts. Outstanding principal balances. Property details including registration particulars.

Section 80EE applies to loans up to ₹35 lakhs for properties valued up to ₹50 lakhs. Section 80EEA covers affordable housing loans up to ₹45 lakhs for properties up to ₹45 lakhs. The distinction matters for eligibility, and the ITR forms now require specific section identification.

Home loan documentation typically spans decades. Maintaining these details throughout the loan tenure becomes crucial—not just for current year filing but for ongoing compliance.

Electric Vehicle Loans: Section 80EEB

Section 80EEB represents the government’s push toward clean energy adoption. The deduction itself is relatively new, and now the documentation requirements match other loan-based deductions.

EV loan details mirror housing loan requirements. Lender institutions, loan account numbers, vehicle specifications, sanction dates, principal amounts, outstanding balances.

The connection between loan purpose and vehicle purchase needs clear documentation. Vehicle registration certificates, loan agreements, purchase invoices—all become relevant for establishing the EV loan claim.

Up to ₹1.5 lakhs deduction on interest paid. The limit is generous, but the documentation requirements ensure legitimate claims. Though honestly, most EV loans today don’t generate interest amounts anywhere near that limit.

Specified Disease Treatment: Section 80DDB

Medical treatment deductions under Section 80DDB now require disease-specific identification. This change feels necessary given the nature of the claims, though it adds complexity for families dealing with serious medical conditions.

Specified disease names—exact medical conditions as per the prescribed list. Medical practitioner details including qualifications and registrations. Treatment institution names. Expense breakdowns covering treatment costs, medicines, related expenses.

Medical certificates from specialist doctors become mandatory. The prescribed diseases list includes cancer, kidney disorders, HIV/AIDS, chronic renal failure, neurological diseases—conditions where treatment costs can be substantial.

Deduction limits are ₹40,000 for individuals below 60 years, ₹1,00,000 for senior citizens. The enhanced documentation requirements ensure claims align with actual medical expenses for specified conditions.

The Practical Side of Compliance

These ITR-1 and ITR-4 additional disclosure requirements for AY 2025-26 demand systematic record-keeping throughout the financial year. Waiting until filing season to gather documents creates unnecessary stress and potential errors.

I’d recommend creating separate digital folders for each deduction category. Policy numbers, account statements, institutional details, receipt numbers—all organized and easily accessible.

The department’s verification capabilities have improved significantly. Cross-checking with banks, insurance companies, lending institutions happens more efficiently now. Accurate documentation becomes your first line of defense against assessment queries.

Sometimes I wonder if these changes will actually streamline the process or create more bottlenecks. Enhanced scrutiny capabilities should theoretically lead to faster processing for compliant taxpayers and stricter oversight for discrepancies.

But implementation rarely matches theory perfectly.

Documentation Strategy Moving Forward

Start organizing immediately if you haven’t already. The transition from amount-based reporting to document-specific disclosures requires adjustment in how we maintain tax records.

Digital copies of relevant documents, policy numbers, account statements, institutional details—all need systematic organization. Physical documents can get lost or damaged, but digital backups provide security.

Consider using cloud storage for tax documents. Accessibility from multiple devices helps during ITR preparation, especially when working with tax professionals or family members who assist with filing.

The enhanced disclosure requirements represent significant evolution in tax compliance expectations. Initially challenging, yes. But potentially leading to more accurate reporting and efficient tax administration over time.

Though that remains to be seen.

Moving Forward with Enhanced Disclosures

The ITR-1 and ITR-4 additional disclosure requirements for AY 2025-26 mark important changes for old regime taxpayers. These modifications demand meticulous documentation and systematic record-keeping practices.

Success lies in proactive preparation and understanding specific documentation needs for each deduction category. The department’s emphasis on detailed disclosures signals movement toward greater transparency and accountability in tax compliance.

Whether this improves the overall system or creates new complications—well, we’ll find out during the filing season.

For comprehensive guidance on ITR-1 and ITR-4 additional disclosure requirements for AY 2025-26 and tax planning strategies, TaxGroww provides expert assistance to ensure accurate compliance with evolving regulatory changes. Professional support becomes invaluable when navigating complex documentation requirements and changing tax landscapes.