Table of Contents

Introduction

For many small business owners and professionals in India, maintaining detailed books of accounts and undergoing tax audits can be burdensome, time-consuming, and often requires professional assistance that comes at a significant cost. Recognizing these challenges, the Income Tax Act introduced the presumptive taxation scheme under sections 44AD, 44ADA, and 44AE to simplify tax compliance for eligible taxpayers.

These provisions allow qualifying taxpayers to declare income at predetermined rates based on their turnover or gross receipts, eliminating the need for detailed bookkeeping and mandatory tax audits. This taxpayer-friendly approach aims to reduce compliance costs while ensuring that the tax net captures smaller businesses and professionals who might otherwise find it difficult to comply with complex tax regulations.

This article provides a detailed analysis of the presumptive taxation scheme, examining each section’s provisions, benefits, limitations, and recent updates to help taxpayers make informed decisions about their tax planning strategies.

Understanding Presumptive Taxation: The Concept

Presumptive taxation is based on the principle of estimating income rather than computing it through detailed financial records. The Income Tax Act presumes a certain percentage of turnover or gross receipts as taxable income for eligible taxpayers, based on the nature of their business or profession.

This approach serves multiple purposes:

- Simplification: It reduces the compliance burden on small taxpayers

- Cost-effectiveness: It eliminates the need for professional accounting services

- Certainty: It provides a clear framework for income computation

- Widening tax base: It encourages voluntary tax compliance among small businesses

The Act currently provides three distinct presumptive taxation schemes under sections 44AD, 44ADA, and 44AE, each catering to different categories of taxpayers.

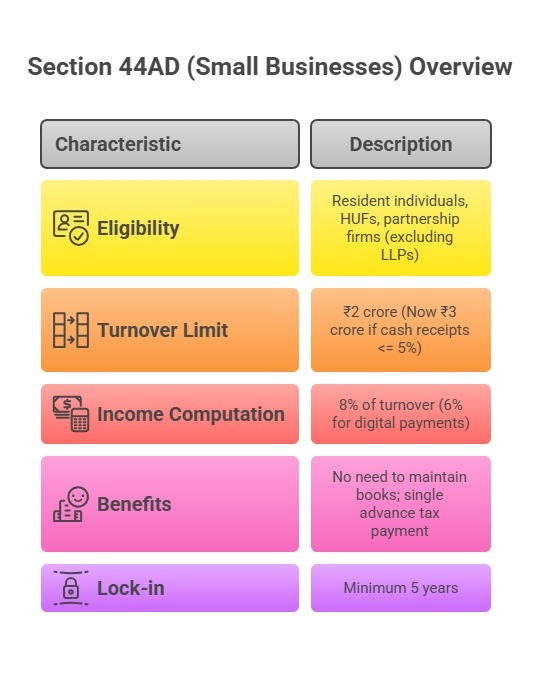

Section 44AD: Presumptive Taxation Scheme for Small Businesses

Eligibility Criteria

Section 44AD applies to:

- Resident individuals

- Resident Hindu Undivided Families (HUFs)

- Resident partnership firms (excluding Limited Liability Partnerships)

This scheme is specifically not available to:

- Non-resident individuals or entities

- Companies (including private and public limited companies)

- Limited Liability Partnerships (LLPs)

- Any taxpayer who has claimed deductions under sections 10A, 10AA, 10B, 10BA, or under sections 80HH to 80RRB in the relevant assessment year

Turnover Threshold

The eligibility threshold for section 44AD has been significantly enhanced:

- Old Standard threshold: Total turnover or gross receipts not exceeding ₹2,00,00,000 in the previous year

- Enhanced threshold: ₹3,00,00,000 if the amount of cash receipts during the previous year does not exceed 5% of the total turnover or gross receipts w.e.f 01/04/2024.

This digital payment incentive was introduced to encourage cashless transactions and financial transparency.

Income Computation

Under section 44AD, the presumptive income is calculated as follows:

- 8% of the total turnover or gross receipts for businesses in general

- 6% of the total turnover or gross receipts for amounts received through banking channels (including digital payments) example Account payee cheque, Online Bank Transfer, RTGS, NEFT, UPI etc.

This two-tier structure provides an incentive for businesses to adopt digital payment methods.

Example of Income Computation under Section 44AD

Scenario 1: Mr. Sharma runs a retail business with annual turnover of ₹1,80,00,000, out of which ₹1,70,00,000 is received through digital means and ₹10,00,000 in cash.

Cash receipts percentage: (₹10,00,000/₹1,80,00,000) × 100 = 5.56%

Since cash receipts exceed 5% of total turnover, the entire income will be calculated at 8%.

Presumptive income: 8% of ₹1,80,00,000 = ₹14,40,000

Scenario 2: Mrs. Patel has a wholesale business with annual turnover of ₹2,50,00,000, out of which ₹2,40,00,000 is received through banking channels and ₹10,00,000 in cash.

Cash receipts percentage: (₹10,00,000/₹2,50,00,000) × 100 = 4%

Since cash receipts are less than 5% of total turnover and the turnover is below ₹3,00,00,000, she is eligible for section 44AD.

Presumptive income: 6% of ₹2,40,00,000 (digital receipts) + 8% of ₹10,00,000 (cash receipts) = ₹14,40,000 + ₹80,000 = ₹15,20,000

Maintenance of Books of Account

A significant advantage of opting for the section 44AD scheme is exemption from maintaining books of accounts under section 44AA. This relieves small business owners from:

- Maintaining day-to-day books of accounts

- Preparing profit and loss statements

- Maintaining asset registers

- Preparing balance sheets

However, it is advisable to maintain basic records of transactions for personal reference and to substantiate claims if required by tax authorities.

Advance Tax Payment

Taxpayers opting for section 44AD enjoy a simplified advance tax payment schedule. Unlike the regular quarterly installment system, they are required to pay the entire advance tax in a single installment on or before March 15th of the financial year.

Failure to pay advance tax by the due date will attract interest under section 234C.

The Lock-in Period

One of the critical aspects of section 44AD is the lock-in period. Once a taxpayer opts for the presumptive taxation scheme and has income exceeding the basic exemption limit, they must continue with this scheme for five consecutive assessment years. If they opt out before completing five years, they:

- Cannot avail the benefit of section 44AD for the next five assessment years

- Must maintain books of accounts as per section 44AA

- Must get their accounts audited under section 44AB if their turnover exceeds the specified limits

This provision aims to ensure consistency in tax compliance and prevent taxpayers from switching between normal and presumptive taxation schemes arbitrarily.

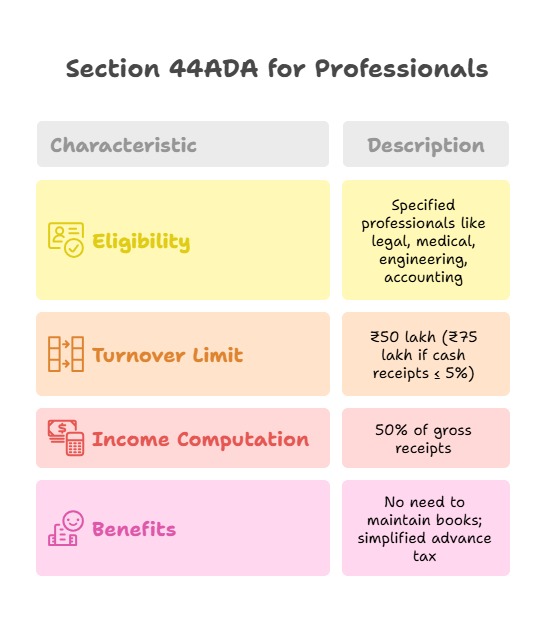

Section 44ADA: Presumptive Taxation for Professionals

Eligibility Criteria

Section 44ADA, introduced in the Finance Act 2016, extends the benefit of presumptive taxation to specific professionals. As of May 2025, the scheme applies to resident individuals, partnership firms (not LLPs), and HUFs engaged in the following professions:

- Legal practice

- Medical practice

- Engineering or architectural services

- Accountancy services

- Technical consultancy

- Interior decoration

- Any other profession as notified by the Central Board of Direct Taxes (CBDT)

Turnover Threshold

The turnover threshold for section 44ADA has seen significant changes:

- Standard threshold: Gross receipts not exceeding ₹50,00,000 in the previous year

- Enhanced threshold: ₹75,00,000 if the amount of cash receipts during the previous year does not exceed 5% of the total gross receipts w.e.f 01/04/2023.

An important clarification made in the 2024 Finance Act is that receipts through non-account payee cheques or drafts are considered as cash receipts for the purpose of determining eligibility under the enhanced threshold.

Income/Profit Computation

Under section 44ADA, the presumptive income is fixed at:

- 50% of the total gross receipts of the profession

This means that a professional with gross receipts of ₹40,00,000 would have a presumptive income/Profit of ₹20,00,000.

Professionals can also declare income higher than the presumptive rate if their actual income exceeds 50% of gross receipts. This provision allows professionals with lower profit margins to still benefit from the simplified compliance regime.

Advance Tax and Books of Account

Similar to section 44AD, professionals opting for section 44ADA:

- Are required to pay advance tax in a single installment by March 15th of the financial year

- Are exempt from maintaining books of accounts under section 44AA

- Are not required to get their accounts audited under section 44AB

Practical Application of Section 44ADA

Example: Dr. Gupta, a medical practitioner, has gross receipts of ₹65,00,000 for FY 2024-25, with 97% of payments received through digital means.

Analysis:

- Since cash receipts are less than 5% of total receipts and gross receipts are below ₹75,00,000, Dr. Gupta is eligible for section 44ADA

- Presumptive income: 50% of ₹65,00,000 = ₹32,50,000

- Dr. Gupta is exempt from maintaining detailed books of accounts

- He must pay advance tax on ₹32,50,000 by March 15, 2025

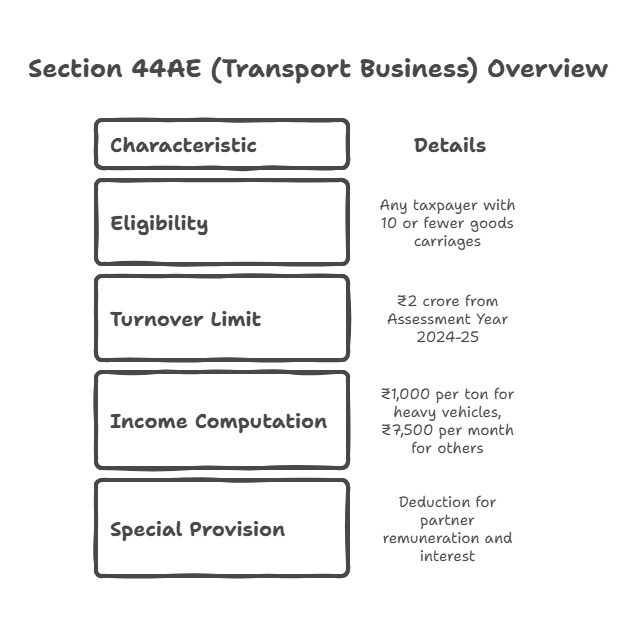

Section 44AE: Presumptive Taxation for Transport Business

Eligibility Criteria

Section 44AE provides a presumptive taxation scheme specifically designed for transporters. Unlike sections 44AD and 44ADA, this scheme is available to all types of taxpayers (individuals, HUFs, firms, companies, etc.) engaged in the business of plying, hiring, or leasing goods carriages.

The key eligibility criterion is:

- The taxpayer should not own more than 10 goods carriages at any time during the previous year

Turnover Threshold

A unique aspect of section 44AE is that it does not prescribe any turnover limit for eligibility. Instead, it focuses on the number of vehicles owned, irrespective of the total receipts.

However, the Finance Act 2024 introduced an additional cap of ₹2,00,00,000 as the maximum turnover for eligibility under this section, effective from April 1, 2024 (Assessment Year 2024-25 onwards).

Income Computation

The presumptive income under section 44AE is calculated as follows:

- For heavy goods vehicles (gross vehicle weight exceeding 12,000 kg):

- ₹1,000 per ton of gross vehicle weight (or part thereof) for every month (or part of a month) during which the vehicle is owned by the taxpayer

- For other goods vehicles (gross vehicle weight not exceeding 12,000 kg):

- ₹7,500 per vehicle for every month (or part of a month) during which the vehicle is owned by the taxpayer

Example of Income Computation Under Section 44AE

Scenario: Mr. Singh owns 8 goods vehicles throughout FY 2024-25:

- 5 heavy goods vehicles with gross vehicle weight of 15 tons each

- 3 medium goods vehicles with gross vehicle weight of 8 tons each

Computation for heavy goods vehicles: 5 vehicles × 15 tons × ₹1,000 × 12 months = ₹9,00,000

Computation for medium goods vehicles: 3 vehicles × ₹7,500 × 12 months = ₹2,70,000

Total presumptive income: ₹9,00,000 + ₹2,70,000 = ₹11,70,000

This income is considered the final taxable income from the transport business, and no further deductions are allowed for expenses incurred.

Advance Tax and Books of Account

Unlike the other presumptive taxation schemes:

- Section 44AE does not provide any concession regarding advance tax payment. Transporters must pay advance tax in regular quarterly installments as applicable to other taxpayers.

- Transporters opting for section 44AE are exempt from maintaining books of accounts under section 44AA and from tax audit under section 44AB for their transport business.

Special Provision for Partnership Firms

In the case of a partnership firm opting for section 44AE, after computing the presumptive income, the firm can claim further deductions for:

- Remuneration paid to partners (subject to limits specified in section 40(b))

- Interest paid to partners (up to 12% per annum as per section 40(b))

This is a unique feature not available under sections 44AD and 44ADA.

Comparison of Three Presumptive Taxation Schemes

Parameter | Section 44AD | Section 44ADA | Section 44AE |

Applicable to | Small businesses | Specified professionals | Transport business |

Eligible taxpayers | Resident individuals, HUFs, partnership firms (not LLPs) | Resident individuals, partnership firms (not LLPs), HUFs | All taxpayers (with ≤10 goods carriages) |

Turnover limit | ₹2,00,00,000 (₹3,00,00,000 if cash receipts ≤5%) | ₹50,00,000 (₹75,00,000 if cash receipts ≤5%) | ₹2,00,00,000 (w.e.f. AY 2024-25) |

Presumptive rate | 8% (6% for digital receipts) | 50% | ₹1,000 per ton for heavy vehicles; ₹7,500 per month for others |

Advance tax | Single payment by March 15th | Single payment by March 15th | Regular quarterly installments |

Books of account | Not required | Not required | Not required |

Lock-in period | 5 years | No specified lock-in | No specified lock-in |

Common Provisions Across All Schemes

Treatment of Depreciation

All three presumptive taxation schemes share a common approach to depreciation:

- Separate deduction for depreciation is not available when computing income under these schemes

- However, the written down value (WDV) of assets is calculated as if depreciation has been claimed and allowed

This ensures continuity in asset valuation even if the taxpayer switches from presumptive to regular taxation in future years.

Higher Income Declaration

Taxpayers can always declare income higher than the presumptive rates if their actual profits are higher. This voluntary compliance option encourages honest tax reporting.

Tax Audit Exemption

Taxpayers declaring income as per the presumptive rates are exempt from tax audit under section 44AB, regardless of their turnover or gross receipts.

However, if a taxpayer declares income lower than the presumptive rate and their turnover exceeds the specified limits (₹1 crore for businesses and ₹50 lakhs for professionals), they must get their accounts audited.

Strategic Considerations for Taxpayers

When to Opt for Presumptive Taxation

Presumptive taxation schemes are particularly beneficial for:

- Businesses with high profit margins: If actual profits exceed the presumptive rates, these schemes offer tax benefits along with compliance simplicity

- Taxpayers with limited resources: Small businesses and professionals without accounting infrastructure can benefit from simplified compliance

- Digital-first businesses: Businesses receiving most payments through banking channels can benefit from the lower 6% rate under section 44AD

When Not to Opt for Presumptive Taxation

These schemes might not be advantageous for:

- Low-margin businesses: If actual profits are significantly lower than the presumptive rates, opting for regular taxation might result in lower tax liability

- Loss-making entities: Losses cannot be claimed under presumptive taxation schemes

- Businesses with significant investments: Capital expenditure cannot be claimed as depreciation under these schemes

- Businesses needing bank loans: Banks often require audited financial statements for loan approval, which might necessitate regular taxation

Impact of Opting Out

The consequences of opting out vary across schemes:

- Section 44AD: Strict 5-year lock-in period with penalties for premature exit

- Section 44ADA: No specific lock-in period mentioned

- Section 44AE: No specific lock-in period mentioned

Compliance Requirements

Tax Return Filing

Taxpayers opting for presumptive taxation must file their income tax returns using:

- ITR-4 (Sugam): For taxpayers covered under sections 44AD and 44ADA

- ITR-4: For taxpayers covered under section 44AE

These returns must be filed by the due date (usually July 31st following the financial year) to avoid penalties.

GST Compliance

It’s important to note that presumptive taxation schemes under the Income Tax Act do not exempt taxpayers from GST compliance. Businesses with turnover exceeding the GST threshold must:

- Register under GST

- File periodic GST returns

- Maintain records as required under GST laws

Documentation Advisable to Maintain

Although detailed books of accounts are not mandatory, it is advisable to maintain:

- Basic record of receipts and payments

- Invoices and bills

- Bank statements

- Asset purchase records

- Vehicle registration and ownership documents (for transporters)

These records can be useful for personal reference and for substantiating claims if questioned by tax authorities.

Practical Case Studies

Case Study 1: Retail Business Owner

Background: Mr. Verma runs a grocery store with annual turnover of ₹2,50,00,000. His actual profit is about 12% of turnover, and 96% of receipts are through digital modes.

Analysis:

- Eligible for section 44AD (turnover below ₹3,00,00,000 with cash receipts less than 5%)

- Presumptive income: 6% of ₹2,40,00,000 (digital) + 8% of ₹10,00,000 (cash) = ₹14,40,000 + ₹80,000 = ₹15,20,000

- Actual profit: 12% of ₹2,50,00,000 = ₹30,00,000

Decision: Mr. Verma should declare his actual profit of ₹30,00,000 rather than the presumptive income, as:

- Higher income declaration is always permitted

- It better reflects his business reality

- It avoids potential scrutiny from tax authorities due to significant deviation from industry averages

He still benefits from simplified compliance without maintaining detailed books or undergoing tax audit.

Case Study 2: Legal Professional

Background: Ms. Sharma, an advocate, has gross receipts of ₹60,00,000 with actual expenses of ₹25,00,000. All receipts are through banking channels.

Analysis:

- Eligible for section 44ADA (receipts below ₹75,00,000 with minimal cash transactions)

- Presumptive income: 50% of ₹60,00,000 = ₹30,00,000

- Actual profit: ₹60,00,000 – ₹25,00,000 = ₹35,00,000

Decision: Ms. Sharma should opt for section 44ADA but declare income of ₹35,00,000 instead of the presumptive ₹30,00,000. This ensures:

- Accurate income reporting

- Compliance simplicity

- No need for detailed bookkeeping

Case Study 3: Transport Business Owner

Background: Mr. Khan owns 7 goods carriages (4 heavy vehicles of 14 tons each and 3 medium vehicles) with annual turnover of ₹1,80,00,000 and actual profit of ₹9,00,000.

Analysis:

- Eligible for section 44AE (owns less than 10 vehicles and turnover below ₹2,00,00,000)

- Presumptive income:

- Heavy vehicles: 4 × 14 tons × ₹1,000 × 12 months = ₹6,72,000

- Medium vehicles: 3 × ₹7,500 × 12 months = ₹2,70,000

- Total = ₹9,42,000

- Actual profit: ₹9,00,000

Decision: Since the presumptive income (₹9,42,000) is slightly higher than his actual profit (₹9,00,000), Mr. Khan has two options:

- Opt for section 44AE for simplified compliance and pay slightly higher tax

- Opt out of presumptive taxation, maintain books of accounts, and pay tax on actual profit

Considering the marginal difference and the compliance burden of regular taxation, section 44AE remains advantageous.

Conclusion

The presumptive taxation schemes under sections 44AD, 44ADA, and 44AE represent the government’s initiative to simplify tax compliance for small businesses, professionals, and transporters. These provisions strike a balance between ensuring tax compliance and reducing the regulatory burden on smaller economic actors.

With the recent enhancements in turnover thresholds and the introduction of digital payment incentives, these schemes have become more attractive to a larger segment of taxpayers. However, the decision to opt for presumptive taxation should be based on a careful analysis of:

- Actual profit margins compared to presumptive rates

- Need for documenting losses or depreciation

- Banking and financing requirements

- Future business expansion plans

- Lock-in implications (especially for section 44AD)

For many small businesses and professionals, these schemes offer a win-win proposition: reduced compliance costs for the taxpayer and wider tax base for the government. As India continues its journey toward formalization and digitization of the economy, presumptive taxation schemes are likely to evolve further, potentially covering more sectors and offering additional incentives for digital transactions.

Taxpayers should regularly review their eligibility and the benefits of these schemes in light of their changing business circumstances and amendments to tax laws. Consulting with a tax professional can provide personalized guidance tailored to specific business needs and help optimize tax planning strategies.

“For the latest Income Tax updates, expert guidance, and comprehensive tax resources, follow Taxgroww.”