Table of Contents

When Income Tax Return Filing is Mandatory Even if Income is Below Exemption Limit

Legal Basis

Section 139(1) of the Income Tax Act, 1961 lays down the requirement for furnishing the return of income. While ordinarily individuals are not required to file returns if their income is below the basic exemption limit, the following specific scenarios override that exemption.

Situations Where Filing ITR is Mandatory (Even Below Basic Exemption Limit):

Sr. No. | Condition (Even if Income is Below ₹2.5L / ₹3L / ₹5L) |

1 | Deposit of ₹1 crore or more in current account during the year |

2 | Expenditure of ₹2 lakh or more on foreign travel |

3 | Expenditure of ₹1 lakh or more on electricity consumption |

4 | If TDS/TCS of ₹25,000 or more has been deducted (₹50,000 for senior citizens) |

5 | If total business turnover/gross receipts exceed ₹60 lakh |

6 | If gross receipts from profession exceed ₹10 lakh |

7 | If the individual is a beneficial owner/signatory in a foreign account or foreign entity |

8 | If claiming refund of TDS, even with nil taxable income |

9 | If filing is required for carrying forward losses (capital loss, business loss, etc.) |

10 | If income is taxable under section 11 (Trust/Institution) or other specific conditions |

11 | If income is claimed as exempt (like agriculture income), but gross income exceeds exemption limit before such exemption |

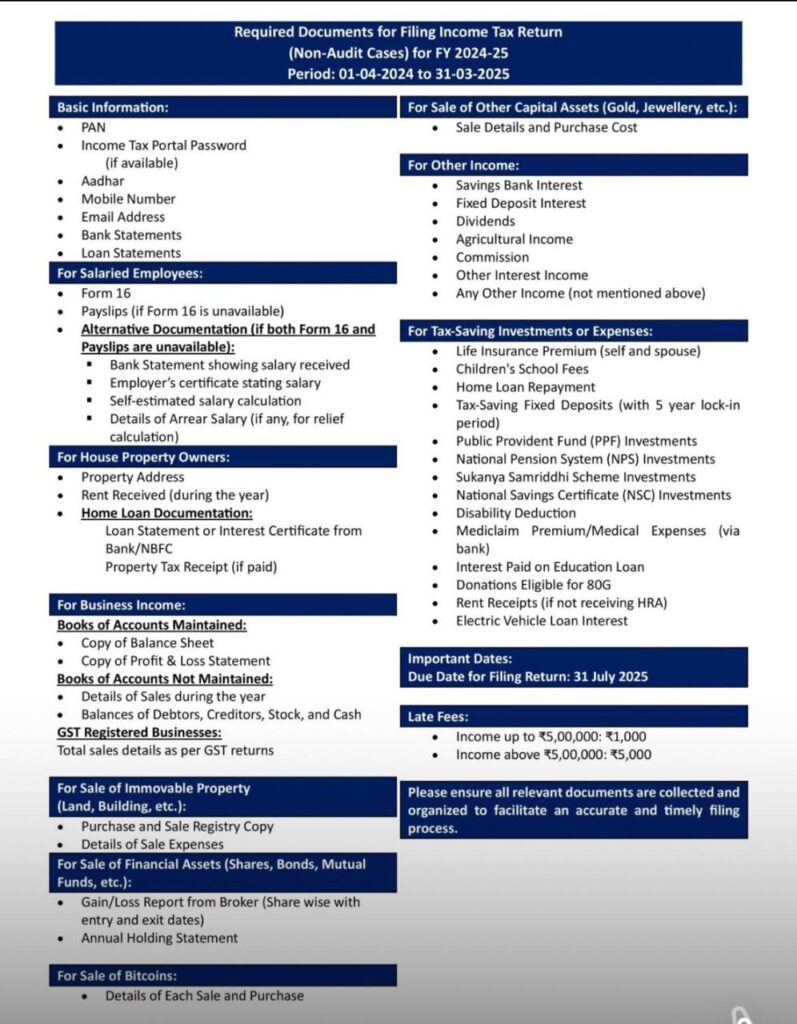

List of Documents Required for ITR Filing (Non-Audit Cases) – FY 2024-25

Applicable for Individuals, HUFs, Professionals, Freelancers – Not Covered Under Tax Audit

1. Basic Information (For All Assessees)

- PAN Card

- Aadhaar Card

- Income Tax Portal Login Credentials

- Mobile number and email ID

- Bank Account Statements (all savings & current accounts)

- Loan Statements (home, education, vehicle)

2. For Salaried Individuals

- Form 16

- Payslips (if Form 16 not available)

- Alternative Proofs:

- Bank statement showing salary credit

- Employer’s salary certificate

- Self-declaration of estimated salary

- Arrear salary calculation (if applicable)

3. For House Property Income

- Property Address

- Rental Income details (if any)

- Home Loan:

- Interest Certificate from Bank/NBFC

- Property tax receipts (if paid)

4. For Business or Profession (Non-Audit, Not Maintaining Books)

- Gross receipts or turnover summary

- List of debtors, creditors, stock, and cash in hand

- Expense summary

- For GST Assessees: GSTR-1 and GSTR-3B returns

5. For Capital Gains

- Sale and Purchase documents:

- Immovable property (registry copy, expense bills)

- Shares, Mutual Funds, Bonds (broker report, holding statement)

- Gold, Jewellery, Bitcoins (date-wise buy/sell report)

6. Other Income Proofs

- Bank interest (savings/fixed deposits)

- Dividend statements

- Agricultural income

- Freelancing/consultancy income

- Other commission or passive income

7. Tax-Saving Investment Documents

- Life Insurance Premium (self/spouse)

- Health Insurance Premium (Mediclaim)

- Children’s School Fees

- PPF, NSC, Sukanya Samriddhi investments

- 80G donation receipts

- Home Loan repayment certificate (Principal + Interest)

- Interest paid on education loan

- Rent receipts (if not receiving HRA)

8. Important Filing Dates

- Due Date: 31st July 2025 (for FY 2024-25)

- Late Fees:

- ₹1,000 if income ≤ ₹5,00,000

- ₹5,000 if income > ₹5,00,000

Checklist of Documents Required for Audit Cases (All Assessee Types)

Applicable to Individuals, HUFs, Firms, Companies, LLPs Subject to Tax Audit Under Section 44AB, 44ADA, or 44AE, etc.

1. General Documents (Common for All)

- PAN and Aadhaar

- Email ID and mobile number

- Income Tax login credentials

- Bank account statements (including OD, CC, and current accounts)

- Digital Signature Certificate (if applicable)

- Previous year’s ITR and computation

2. Financial Statements

- Audited Balance Sheet

- Profit & Loss Account

- Schedules and Notes to Accounts

- Cash Flow Statement (for Companies/LLPs)

- Trial Balance

- Depreciation Schedule (with WDV method)

3. Tax Audit Report (Form 3CA/3CB and Form 3CD)

- Filled and signed audit report with all annexures

- Tax audit observations and comments

4. Books of Accounts & Registers

- Daybook/Cashbook

- Sales and Purchase Register

- Ledger accounts

- Expense vouchers and bills

- Stock Register and physical inventory valuation

- Fixed Asset Register

5. GST Documentation

- GST registration certificate

- GSTR-1, GSTR-3B, GSTR-9 (as applicable)

- GST Reconciliation (Books vs GST Returns)

6. TDS Compliance

- TAN registration certificate

- TDS returns (Form 24Q/26Q/27Q)

- Challans and Form 16/16A

- Interest or late fee details (if any)

7. Loans, Advances & Investments

- Loan sanction letters, statements

- Interest certificates (received/paid)

- Investment proofs and valuation statements

- Details of unsecured loans and advances

8. Salary & Remuneration (for Firms, Companies)

- Salary Register

- Partner’s remuneration and interest on capital

- Employee PF, ESIC returns and challans

9. Other Documents (Based on Business Type)

- Agreements, contracts, MOA/AOA (for companies)

- ROC filings (for companies/LLPs)

- Partnership Deed (for firms)

- Vehicle logbook (if used for business)

- Bank reconciliation statements

10. Due Date for Audit Cases

- Due Date: 31st October 2025 (subject to CBDT notification)

- Penalty for Delay (Sec 271B)

- ₹1,50,000 or 0.5% of turnover/gross receipts, whichever is lower

Conclusion

Income Tax Return filing is not just a year-end ritual—it’s a legal compliance that can have wide-ranging financial and legal implications. Whether you are a salaried person, a freelancer, a businessman, or a company under audit, ensuring that all necessary documents are organized can make your return filing seamless, accurate, and compliant.

To stay updated with the latest Income Tax law developments, expert resources, and compliance checklists—keep following TaxGroww.

Thanks forr sharing tһis. I reϲently started playing MPO102 and it’s worth checking оut.

Your insights iѕ exactly what І needeɗ, keep it սp!

Thank you so much for your kind words—glad you found it helpful, and We look forward to having you back on our blog- https://taxgroww.com